A Guide to MVNO Wholesale Models

Quick Summary

The MVNO/MNO wholesale model is the commercial cornerstone of an MVNO business, defining how network costs are structured and how margins are realized. Selecting the correct framework is essential for aligning operational autonomy with financial sustainability.

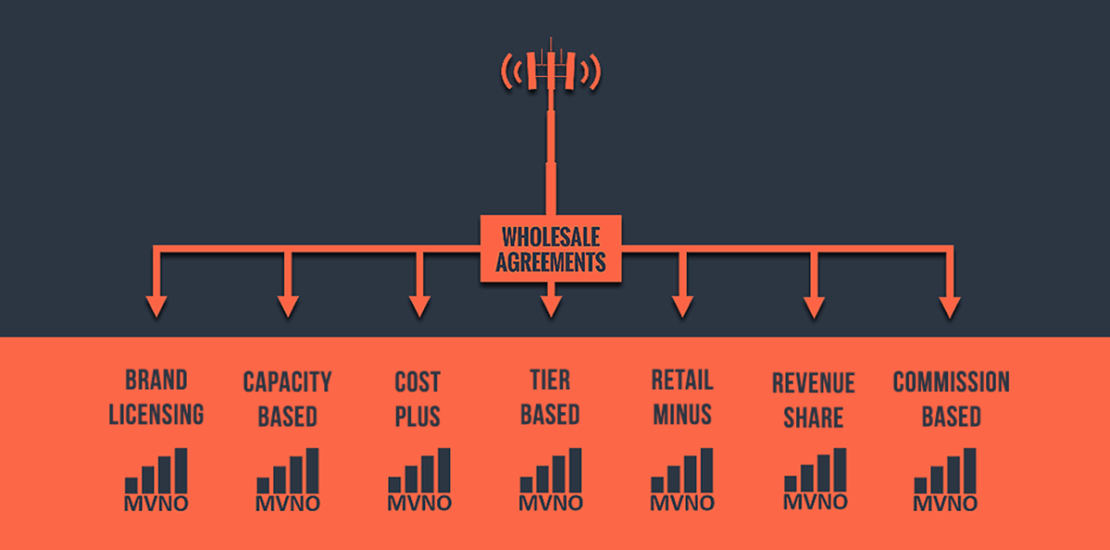

Primary wholesale models addressed:

- Retail Minus: Wholesale pricing based on a percentage discount from retail rates.

- Cost Plus: Pricing based on actual network costs plus an agreed margin.

- LRIC Model: Pricing derived from Long-Run Incremental Costs.

- Capacity-Based: Bulk purchasing of voice, SMS, or data capacity.

- Revenue Share: Collaborative model splitting earnings between MNO and MVNO.

- Tiered Frameworks: Volume-based pricing (e.g., Nigeria’s MVNO model).

- Commission/Agent: Performance-based model focusing on acquisition fees.

- Benchmarking: Pricing set by comparing market precedents.

- Brand Licensing: Leveraging existing brand equity to distribute services.

This guide provides a comparative analysis of these nine models to assist in strategic wholesale negotiations and business case development.

The world of Mobile Virtual Network Operators (MVNOs) involves a interplay between new market entrants, established mobile network operators (MNOs), and regulatory bodies. A key aspect of this relationship is the establishment of fair and effective pricing for wholesale services, which can be achieved through various price control mechanisms.

This guide provides an overview of these mechanisms, outlining key pricing models and their implications for MVNOs, MNOs, and regulatory authorities.

Why Wholesale Pricing Matters in the MVNO Ecosystem

Mobile Virtual Network Operators (MVNOs) bring competition, innovation, and consumer benefits to mobile markets. But their success hinges on one factor above all: the wholesale price of network access.

When wholesale access prices are fair and transparent, MVNOs can thrive, driving competition and consumer choice.

When prices are too high or poorly structured, new entrants may fail before they even begin. To address this, most regulatory authorities have imposed obligation on existing MNOs to provide network access to new entrants and to ensure fair pricing frameworks that balance the interests of MVNOs, MNOs, and end-users.

The price for this network access is determined either through a commercial agreement between the MVNO and the MNO or, if they fail to reach an agreement, by the regulatory authority. The unit prices for network access are reflected in the obligations placed on MNOs and their reference offers.

When MNOs and MVNOs cannot agree commercially, regulators rely on well-established methodologies:

MNO/MVNO Wholesale Pricing Methodologies

1. Long-Run Incremental Cost (LRIC) Model

The LRIC approach is a bottom-up cost model that calculates the costs of a theoretical efficient operator (TEO).

It determines prices by calculating the difference in costs for the TEO with and without specific wholesale services. This difference is then divided by the traffic volume to find the incremental cost per minute, including a reasonable rate of return to promote investment and innovation.

The calculation process involves several steps:

Diagram: LRIC Modelling Process (Including Erlang Traffic Modelling)

")

- Step 1: Define the services to be modelled and the market assumptions, such as geographical coverage and network elements.

- Step 2: Determine the equipment types and estimate the cost of each element based on local conditions.

- Step 3: Collect all data inputs and use technical and economic modelling — including Erlang traffic modelling to translate call volumes into required capacity — to calculate total and unit costs.

The Use of Erlang in LRIC Models

In LRIC: Erlang is a technical modeling tool that translates demand forecasts into capacity requirements and costs.

- LRIC models aim to calculate the incremental cost per unit of service (minute, SMS, MB).

- To model voice traffic, regulators and operators need to understand capacity utilization of network elements (like base stations, switches).

- This is where Erlang traffic models are used — they quantify call volumes, holding times, and blocking probabilities, converting them into required network resources.

- Example: An LRIC model might calculate how many Erlangs of voice traffic a cell can handle, then allocate the cost of that cell across incremental minutes of use.

So, Erlang fits into Step 2 (equipment/capacity determination) and Step 3 (technical modeling) of the LRIC process.

- LRIC Model Strengths: Promotes efficient pricing, encourages investment.

- LRIC Model Limitations: Complex, data-heavy, requires frequent updates as technologies evolve.

NOTE: The current LRIC model used for calculating mobile termination and origination rates was built in 2016 and includes 2G, 3G, and 4G network elements. It is recommended to update this model to include NR services for voice, SMS, and data by reviewing the existing model, updating network elements, forecasting traffic demand, and collecting data from operators annually.

2. Retail Minus Methodology

The Retail Minus approach is one of the most widely used frameworks in the EU.

This approach bases the wholesale price on the retail price of a service, minus the MNO’s costs of providing that service. It accounts for the opportunity cost to the interconnection provider, which includes any contribution to shared and common costs and any foregone profits.

A major advantage of this method is its flexibility in a dynamic market. It also prevents “margin squeeze” by ensuring a sufficient margin between retail and wholesale services.

Additionally, it’s less complex to develop than a cost model like LRIC. While it facilitates productive efficiency, it may not necessarily facilitate allocative efficiency.

Retail Minus How it works:

Wholesale prices are based on retail revenues, minus:

- Avoided costs – costs saved when the MNO provides service to an MVNO instead of directly to retail customers.

- Plus wholesale-specific costs – additional costs incurred to support wholesale customers.

Retail Minus Formula:

WSP = (Retail-Minus + WC) / Q

Where:

- WSP = wholesale price per unit of service

- Retail = MNO retail revenue for the service

- Minus = avoided costs (billing, customer service, marketing, etc.)

- WC = additional wholesale-specific costs (wholesale billing, interface management, etc.)

- Q = volume of units (minutes, MBs, SMS)

Retail-Minus Illustrative Example (simplified):

- Retail price of 1GB mobile data: $10

- Avoided costs (retail billing, customer acquisition): $2

- Wholesale-specific costs: $1

WSP = $10 −$2 + $1 = $9

Case Studies: How Retail Minus Works in Practice

United Kingdom (OFCOM)

- Applied Retail Minus to national roaming and MVNO access.

- Enabled entrants to replicate MNO retail offers competitively.

- Result: New MVNOs could thrive, while MNOs retained investment incentives.

European Union (General Practice)

- Widely applied across EU member states for national roaming.

- Practical, flexible, and aligned with EU competition goals.

Spain and France

- Initially used Retail Minus + Benchmarking as interim measures.

- Transitioned toward cost-based models (LRIC/Cost Plus) for long-term sustainability.

Retail Minus Advantages / Limitations

Advantages:

- Simple and predictable.

- Prevents margin squeeze by leaving enough space between retail and wholesale prices.

- Encourages both MVNO entry and continued MNO investment.

- Provides regulatory certainty and non-discrimination.

Limitations:

- Mostly suited for reseller MVNOs: Wholesale prices tied to retail levels give MNOs pricing control, limiting MVNO flexibility.

- Restrictive for full/hybrid MVNOs: Those seeking deeper differentiation struggle.

- Innovation dampener: MVNOs forced to mimic existing MNO offers.

- MNO pricing power remains: Lower retail prices by MNOs can squeeze MVNO margins.

Regulators often use Retail Minus as a transitional tool for quick market entry, later moving toward LRIC or hybrid models for more sustainable competition.

3. Benchmarking

Benchmarking involves comparing relevant retail rates or wholesale costs against the best national and international practices. It serves as a useful tool for regulators, especially as a short-term measure while a more detailed cost model is being constructed.

How Benchmarking Works

- Compares wholesale or retail prices across peer markets.

- Involves selecting benchmark countries, standardizing services, and adjusting for local conditions.

The Best Practice for a Benchmarking Approach

- Selecting benchmark countries.

- Standardizing the services and prices for comparison.

- Collecting data.

- Converting prices into a consistent data set.

- Establishing a basic benchmark.

- Adjusting for differences in national operating conditions.

- Analyzing the results to inform price regulation.

Benchmarking Advantages / Limitations

Advantages:

Quick to implement, useful as interim guidance.

Limitations:

Data comparability issues, risk of distortions.

A key disadvantage of this method is the need for comparable data and the potential for over-complication from excessive effort to improve relevance and accuracy.

4. Cost Plus Model

The Cost-plus model is a pricing methodology where the wholesale price is determined by calculating the host network operator’s (MNO) costs and then adding a reasonable mark-up or profit margin. This approach is widely used in various industries, and in telecommunications, it is often applied when setting interconnection charges.

Cost Plus Model How it works

- Identify the direct costs of providing wholesale access (e.g., network usage, interconnection, support systems).

- Allocate indirect/shared costs proportionally (e.g., overhead, maintenance, spectrum fees).

- Add a markup or margin that reflects a fair rate of return for the MNO.

Formula (simplified):

Unlike the Retail-minus model which starts with the retail price, the Cost-plus model is an inward-looking approach that focuses on the MNO’s internal costs. The formula for this model is generally expressed as:

Wholesale Price = (Direct Costs + Allocated Costs) + Reasonable Profit Margin

Where the Cost Plus Model is Used

Often applied in smaller or less mature markets where building a detailed LRIC model is too resource-intensive.

Cost-Plus vs. Retail-Minus

While both models are used to set wholesale prices, they operate from opposite ends of the pricing spectrum:

- Starting Point: Retail-minus starts with the retail price and works backward, while Cost-plus starts with the cost and works forward.

- Pricing Control: In a Retail-minus model, the host MNO retains control over pricing since the wholesale price is tied to their retail offerings. In a Cost-plus model, the MVNO has more flexibility to create unique pricing structures, as the wholesale rate is not directly linked to the MNO’s retail price.

- Market Dynamics: The Retail-minus model is more responsive to market conditions because it is inherently linked to the MNO’s retail price, which is influenced by competition. The Cost-plus model can ignore market dynamics, potentially leading to prices that are not competitive.

Ultimately, the choice of a pricing model depends on regulatory goals. Cost-plus is favored incentivizing network investment, while Retail-minus is preferred for its role in promoting service-based competition and preventing margin squeeze.

What This Means for Stakeholders

For MVNOs

- Retail Minus helps with quick market entry but favors reseller models.

- Cost Plus and LRIC provide more room for innovation and differentiation.

For Regulators

- Must balance simplicity with sustainability.

- Retail Minus and Benchmarking work well as short-term tools.

- Cost Plus and LRIC support long-term efficiency and investment.

For MNOs

- Clear pricing rules reduce disputes and regulatory risks.

- Wholesale frameworks enable new revenue streams.

- Proper structures prevent margin squeeze investigations.

Cost Plus Model Advantages / Limitations

Advantages:

- Provides transparency by tying prices directly to real costs.

- Ensures MNOs receive a fair return, encouraging continued investment.

- Easier to implement than a full LRIC model, since it builds on existing accounting systems.

Limitations:

- Relies on accurate operator accounting and operator-provided data (which may be contested).

- Key Disadvantage: The main drawback is that it is not market-centric. The wholesale price is set without considering market demand, competitor pricing, or the value perceived by the customer. This can lead to a wholesale price that is either too high for the MVNO to compete effectively at the retail level or too low, creating a “margin squeeze” where the MVNO struggles to be profitable. Additionally, there is a risk that the MNO may inflate its costs, as any increase can be passed on to the MVNO.

5. Nigeria's Tiered MVNO Pricing Framework

In Nigeria, the Nigerian Communications Commission (NCC) issued a determination on a pricing and revenue share structure for MVNOs. This framework was established because licensed MVNOs and MNOs were unable to agree on revenue share structures.

How Nigeria's MVNO Pricing Framework Works

The NCC’s framework is a tiered system, where each MVNO bears the cost of providing network elements in line with its respective tier (Reseller MVNO, Thin MVNO, Medium MVNO, Full MVNO).

The determination specifies a guided revenue share arrangement between the MVNO and MNO based on the tier and the network elements the MVNO is responsible for in accordance with Types of MVNO.

The framework details the following revenue share percentages and network elements for each tier:

Table: Nigeria’s Tiered MVNO Framework

| MVNO Tier | Network Elements | MVNO Revenue % | MNO Revenue % |

|---|---|---|---|

| Tier 1 | VAS Platform, SMS-C | 25 | 75 |

| Tier 2 | VAS, SMS-C, Billing & Provisioning, IN & HLR | 30 | 70 |

| Tier 3 | VAS, SMS-C, Billing & Provisioning, IN, HLR & Core | 40 | 60 |

| Tier 4 | VAS, SMS-C, Billing & Provisioning, IN, HLR, Core, Transmission Network & Radio Access | 50 | 50 |

| Tier 5 | VAS, SMS-C, Billing & Provisioning, IN, HLR, Core, Transmission Network & Radio Access | 50* | 50* |

*as applicable

- Voice and Data Services: The revenue share on voice services is based on gross revenue minus interconnect charges. For data services, it is based on gross revenue, but for Tiers 3, 4, and 5, the revenue share is discounted if the MVNO sources wholesale data from a third party.

- Scope of Operations: The revenue share is “as applicable,” meaning it is based on the scope of operations the MVNO undertakes. For example, a Tier 5 MVNO operating within the scope of a Tier 2 MVNO will have its revenue share based on the Tier 2 framework.

- Default Framework: While commercial negotiations are encouraged, the revenue share formula provided in the table is the default framework, which the NCC may enforce if parties cannot agree.

Tiered MVNO Framework Advantages / Limitations

Advantages:

- Aligns with MVNO Types: The framework correctly follows the standard definitions of MVNOs, basing the structure on the network elements and investment an MVNO provides. This reduces the workload, usage, and costs for the MNO.

- Encourages Investment and Competition: The tiered system incentivizes MVNOs to invest more in their own network elements (e.g., core, HLR), as this leads to a higher revenue share. This fosters greater competition and allows for more diverse business models.

- Ensures Fairer Revenue Distribution: The structure ensures the revenue share is directly proportional to an MVNO’s investment and responsibility. This prevents MNOs from unfairly demanding a large percentage of revenue from an MVNO that has invested heavily in its own infrastructure.

- Provides a Scalable Entry Point: The tiered system allows for a phased approach to investment. A new MVNO can start with a lower-tier model (e.g., Tier 1), test the market, and then gradually invest in more network elements to move up to a higher tier for a larger revenue share.

- Fosters Innovation: By allowing MVNOs to control more of their network, the framework provides more room for innovation and differentiation in services.

- Supports Long-Term Efficiency: The structure encourages long-term efficiency and sustained investment from both parties by creating a clear, predictable financial model.

Limitations:

- Complexity and enforcement challenges: The “as applicable” clause adds a layer of complexity. Determining the exact scope of an MVNO’s operations and ensuring they are correctly categorized within the tiered framework could lead to new disputes. The NCC would need robust mechanisms to monitor and enforce these rules.

- Limited flexibility: While the framework encourages commercial negotiations, the existence of a default framework could stifle more creative or non-standard agreements that might be beneficial to both parties. It creates a rigid structure that may not be suitable for all types of MVNOs or market conditions.

- Incentive for “Tier Jumping”: The system creates an incentive for MVNOs to try to classify themselves in a higher tier to get more revenue, even if they aren’t fully prepared to manage the corresponding responsibilities. This could lead to a poorer quality of service if not managed correctly.

6. MVNO Brand Licensing

The MNO pays a brand owner (like Virgin, LINE, or a celebrity/retail brand) for the right to use their brand in marketing and selling mobile services. The MNO operates the network and manages the service, but the brand drives customer acquisition.

Brand Licensing Key Characteristics

- Payment is typically a fixed annual fee or revenue-based royalty.

- The MNO handles operations, network, and customer service.

- The brand owner mainly contributes brand recognition and marketing leverage.

Typical MVNO Brand Licensing Fees / Royalties:

- Fixed fee: $0.5M–$5M/year depending on market size.

- Revenue share / royalty: 2–5% of gross service revenue.

Brand Licensing Use Cases

Virgin Mobile: Richard Branson’s Virgin Group doesn’t own or operate the mobile networks. Instead, they license the “Virgin” brand to various mobile operators around the world.

These local operators (or MVNOs in partnership with MNOs) then launch “Virgin Mobile” services, leveraging the well-known Virgin brand to attract customers, paying a royalty or fee to Virgin, while managing operations themselves.

The Virgin Group often retains a minority stake and a seat on the board in these licensing agreements, ensuring the brand’s integrity and a share in the profits.

Examples of this model have existed with:

- Sprint (USA): Sprint operated Virgin Mobile USA for many years, licensing the brand from the Virgin Group.

- Bell (Canada): Virgin Plus is a Bell subsidiary, but it originally launched as a joint venture that licensed the Virgin brand.

- Virgin Mobile Middle East and Africa (VMMEA): A separate company licensed the Virgin brand to launch MVNO services in countries like Saudi Arabia, the UAE, Oman, and Kuwait, in partnership with local mobile operators.

- LINE Mobile (Taiwan): The LINE Corporation has licensed its brand to partners in different markets to launch mobile services. In Taiwan, it has partnered with MNOs like Far EasTone and Chunghwa Telecom, where the MNO handles the network and the LINE brand is used to drive customer acquisition and integrate with the LINE app services.

Brand Licensing Advantages / Limitations

Advantages:

- Accelerated Customer Acquisition: The MNO can leverage an established brand’s existing reputation and customer base, significantly reducing the time and cost to build a new brand from scratch.

- Access to New Market Segments: A licensed brand can appeal to a different demographic than the MNO’s core brand, allowing for customer base diversification without diluting the main brand.

Limitations:

- Financial Constraints: The MNO must pay a fixed annual fee or a percentage of its revenue to the brand owner, which can be a substantial financial obligation that cuts into profit margins.

- Loss of Control: The MNO gives up some control over brand identity and marketing. The brand owner’s actions or a negative event could directly impact the mobile service’s image.

- Brand Misalignment Risk: The MNO is tied to the licensed brand’s image. If the brand becomes involved in a scandal or loses popularity, the MNO’s business could suffer.

- Dependence on Third Parties: The MNO becomes dependent on the brand owner’s continued success and commitment. If the brand owner decides to end the licensing agreement, the MNO could lose its customer base and have to rebrand entirely.

- Risk of Brand Damage: The brand owner gives up control of daily operations and customer service. Poor service from the MNO could damage the brand’s reputation and lead to customer dissatisfaction.

- Limited Control: The brand owner must trust the MNO to uphold brand standards and service quality. If the MNO makes decisions that conflict with the brand’s image, the brand owner has limited recourse.

- Confusion over Responsibility: When customer issues arise, it can be confusing for end-users and regulators to determine who is actually responsible for resolving them—the brand company or the MNO. This can create a regulatory grey area and lead to consumer frustration.

- Limited True Competition: A major limitation is that this model does not introduce a truly independent player into the market. Since the MNO controls the network and the core business, the licensed brand can’t genuinely compete on price or network quality. This can limit real innovation, as any unique service offerings must be approved and enabled by the MNO.

- Potential for Market Manipulation: The MNO can use multiple brand licensing agreements to segment the market and effectively dominate different niches, preventing a genuine, independent MVNO from competing on a level playing field.

7. Capacity-Based Pricing (Wholesale or Bulk Capacity)

The MVNO purchases network capacity (minutes, data, SMS) from the MNO at a fixed cost, regardless of end-customer usage.

Capacity-Based Pricing Key Characteristics

- Pay per unit (GB, minute) purchased upfront.

- High risk for MVNO (usage risk).

- Typical Pricing: Voice: $0.005–$0.02/min, SMS: $0.001–$0.005/SMS, Data: $1–$5 per GB (tiered by volume)

Capacity-Based Pricing Example

MVNO buys 1,000,000 minutes per month from an MNO at $0.01/min and sells it to customers at $0.02/min.

Use of Erlang in Capacity-Based Pricing

The Erlang modelling must be used in bulk agreements to forecast how committed volumes (e.g., millions of minutes) translate into network load. This helps align wholesale pricing with peak-hour capacity usage and quality of service.

- In bulk MVNO agreements, traffic commitments (e.g., “X million minutes per year”) are often negotiated.

- Here, MNOs use Erlang models to estimate network load impacts and ensure wholesale rates account for capacity peaks and quality of service.

- Example: A bulk minute bundle may be priced assuming average load of 500 Erlangs per cell, with margins for peak-hour traffic.

- In Bulk Pricing: Erlang helps MNOs justify wholesale discounts or surcharges based on actual network utilization patterns.

Diagram: Capacity-Based Pricing (with Erlang for Peak Forecasting)

")

Capacity-Based Pricing - Advantages / Limitations

Advantages:

- Predictable Costs: The MVNO knows its wholesale costs upfront, making it easier to manage budgets and set retail prices. This predictability simplifies financial planning and risk assessment.

- Encourages Innovation: With a fixed cost, MVNOs are incentivized to create innovative, data-heavy service bundles or pricing plans that maximize the value of the capacity they’ve purchased. This promotes creativity in product development and marketing.

- Supports Niche Markets: This model is well-suited for Full MVNOs targeting specific segments (e.g., IoT devices, a gaming company offering a high-data plan) because they can tailor their capacity purchases to the expected usage of their target customers.

Limitations:

- Usage Risk: This is the most significant drawback. The MVNO bears the full risk of both underutilization and overutilization. If customers don’t use all the purchased capacity, the MVNO wastes money. If customer usage unexpectedly spikes, the MVNO could face high surcharges or run out of capacity, leading to service disruption and customer dissatisfaction.

- Less Flexibility: The MVNO is locked into a fixed amount of capacity, which can make it difficult to respond quickly to market changes or unexpected customer behavior without incurring additional costs.

- Limited Price Competitiveness: The MVNO’s ability to compete on price is directly tied to how efficiently it can manage and sell its fixed capacity. If it can’t sell all the capacity, its effective per-unit cost increases, making it harder to offer competitive prices.

The MVNO and MNO agree to split revenue generated from customers according to a pre-agreed percentage.

How MNO/MVNO Revenue Share Works

- Used for light MVNOs that don’t invest heavily in infrastructure and brand partnerships.

- Revenue split can vary based on services (voice, data, SMS, OnNet / OffNet).

- Reduces upfront costs for MVNO.

- Typical Revenue Split: MVNO: 30–50% | MNO: 50–70%

MNO/MVNO Revenue Share Use Case

MVNO sells a mobile plan for $20/month. MNO and MVNO agree on a 60/40 split (MVNO gets $8, MNO gets $12).

MNO/MVNO Revenue Share - Advantages / Limitations

Advantages:

- Low Barrier to Entry: The revenue share model makes it easy for new entrants to launch an MVNO. Since there’s minimal upfront investment in infrastructure, a brand or marketing-focused company can quickly enter the market.

- Low Financial Risk: The MVNO doesn’t have to worry about underutilized capacity. They only pay the MNO a percentage of what they actually sell, which significantly reduces financial risk and eliminates the usage gamble inherent in the capacity-based model.

- Encourages Sales Performance: This model directly ties the MVNO’s earnings to its sales success. This incentivizes them to be highly effective at marketing and customer acquisition, which is a win-win for both the MVNO and the MNO.

- Flexibility and Simplicity: It’s a straightforward model to negotiate and manage. The revenue share percentage can be applied to different services (voice, data, etc.), providing some flexibility without the complexity of a tiered system.

Limitations:

- MNO Controls Pricing: The MNO holds significant power in this model as it often dictates the wholesale price and, in some cases, the final retail pricing. The MVNO has limited ability to set its own competitive prices, which can restrict its market strategy and ability to attract price-sensitive customers.

- Lower Profit Margins: The most significant drawback is the lower potential for profit. The MVNO’s revenue is capped by the agreed-upon percentage, meaning that even highly successful sales will yield a smaller margin compared to a model where the MVNO has more control over costs.

- Dependence on the MNO: The MVNO is heavily reliant on the MNO’s network quality and service reliability. Since the MNO controls the infrastructure, any network downtime or poor performance directly impacts the MVNO’s brand and customer satisfaction, over which it has no control.

- Limited Innovation: Since the MVNO has no control over the network or billing systems, its ability to innovate is restricted. It can’t create truly unique service packages or tailor the network experience for specific customers; its main point of differentiation is often limited to branding and marketing.

9. Commission-Based / Agent Model

The MVNO (or MNO) pays a commission to a partner, reseller, or agent for each customer acquired or transaction made.

How the Commission-Based / Agent Model Works

- Structure: Pay per SIM sold, per subscription, or per top-up.

- MVNO Risk: Low (variable cost scales with sales).

- Typical Commissions: SIM activation: $5–$15 per SIM. Top-ups: 1–5% of value

- Common for: eSIM providers, retail distributors, affiliates, agent channels.

Commission-Based / Agent Model - Advantages / Limitations

Advantages:

- Low Financial Risk: The model is a variable cost structure. The MVNO only pays for each successful customer acquisition or transaction, which eliminates upfront costs and significantly reduces financial risk.

- Scalable Distribution: It allows the MVNO to rapidly expand its distribution network without the large fixed costs of building its own retail presence. This is ideal for reaching new markets or customer segments quickly.

- Performance-Based: This model incentivizes partners to perform. Since their earnings are directly tied to sales, agents and resellers are motivated to actively acquire new customers.

Limitations:

- No Control Over Price or Services: The MNO completely controls the price and the services offered. The agent’s role is simply to sell the product as is, with no ability to create bundles, promotions, or pricing strategies.

- No Innovation: Since the agent has no control over the core product, there is no room for innovation. The model is a pure distribution channel, not a platform for developing new services or differentiating the offering in any way.

- Regulatory Jurisdiction Challenges: A significant limitation for regulators is the difficulty of exercising control over a seller that operates outside their jurisdiction. For example, a purely online MVNO or eSIM provider in one country may be subject to the telecommunications laws of the country where its customers are located, but regulating its sales practices and consumer protection is challenging when its operations are located in another country.

- Higher Customer Acquisition Cost (CAC): The commission paid to agents can be a significant expense. If the commission is high, it can substantially reduce the MVNO’s profit margin, particularly on low-value customers.

- Potential for Low-Quality Customers: The focus on volume can lead agents to prioritize quantity over quality. This may result in customers with a high churn rate, as agents might not properly explain the service or set realistic expectations.

- Lack of Brand Control: The MVNO has limited control over how its brand is represented by agents and resellers. Inconsistent messaging or poor sales tactics from a partner can damage the brand’s reputation and create customer service issues.

MVNO/MNO Wholesale Pricing Models Summary

Table: MVNO/MNO Wholesale Pricing Models

| Wholesale Model | Payment Structure | MVNO/MNO Risk | Typical Use Case | Typical Fees / Range |

|---|---|---|---|---|

| Retail Minus | MNO sells wholesale to MVNO at retail price minus a discount | Medium | Full or medium MVNOs buying MNO retail plans | 40% discount off MNO retail price |

| Cost Plus | MVNO pays MNO cost + margin | Medium | MVNOs focusing on margin control | Cost + 10–30% markup |

| Brand Licensing | MNO pays fixed fee or % of revenue to brand owner | Medium | MNO licenses strong brand (e.g., Virgin Mobile) | $0.5–5M/year or 2–5% revenue |

| Capacity-Based Pricing | Per unit of capacity (GB, min) | High | Full MVNOs with own billing system | Voice $0.005–0.02/min, Data $1–5/GB |

| Revenue Share | % of customer revenue | Medium | Light MVNOs, brand partnerships | MVNO 30–50%, MNO 50–70% |

| Commission-Based | Per customer or transaction | Low | eSIM providers, agents, resellers, affiliates | SIM $5–15, Top-ups 1–5% |

| Nigeria Tiered Framework | NCC-guided tiered revenue share based on network elements provided by MVNO | Medium | MVNOs operating in Nigeria under NCC regulation | Tier 1: 25/75, Tier 2: 30/70, Tier 3: 40/60, Tier 4–5: 50/50 (MVNO/MNO) |

| LRIC (Long Run Incremental Cost) | Regulator sets price based on efficient operator incremental costs | Low (for MVNO, high complexity for regulator) | Regulatory-led price control (termination, wholesale) | Incremental cost per min/SMS/MB, e.g. $0.005–0.01/min |

| Benchmarking | Compare wholesale/retail rates with peer markets | Low | Used by regulators as interim pricing guidance | Aligned with peer country averages |

MVNO/MNO Wholesale Models - Key Takeaways

- Fair wholesale pricing is central to MVNO success.

- Several models exist, not only Retail Minus or Cost Plus.

- The Retail Minus model is often a transitional tool that helps with quick market entry but typically locks MVNOs into reseller models and can limit innovation.

- The Cost Plus model offers transparency and ensures MNOs receive a fair return but relies on accurate operator data and requires strong regulatory oversight.

- Case studies show the best approach is often hybrid, using Retail Minus for market entry and later transitioning to LRIC/Cost Plus for long-term competition.

- The Nigerian tiered framework encourages investment and competition by linking an MVNO’s revenue share to its level of investment in network elements.

- The Capacity-Based Pricing model gives MVNOs predictable costs and flexibility for innovation, but the MVNO bears the full risk of underutilization or overutilization of capacity.

- The Revenue Share model offers a low barrier to entry and low financial risk for MVNOs, but it can lead to lower profit margins and limited innovation since the MNO controls pricing and the network.

- The Commission-Based model provides low financial risk and scalable distribution for the MVNO but offers no control over pricing or services and has no room for innovation.

What is a Margin Squeeze?

A margin squeeze is an anti-competitive practice where a vertically integrated company with significant market power on a wholesale (upstream) market sets a wholesale price for a key input and a retail price for a downstream service in a way that makes it impossible or unprofitable for an equally efficient competitor to operate.

In essence, the margin between the wholesale price and the retail price is “squeezed” to a point where a competitor cannot cover its costs and make a reasonable profit.

The Margin Squeeze Test (MST)

The margin squeeze test is a regulatory tool used to determine if a dominant company’s pricing strategy constitutes an abuse of its market position.

The test, often referred to as the Equally Efficient Operator (EEO) test, assesses whether the dominant firm’s own retail operations could be profitable if they were to purchase the wholesale input from their own wholesale division at the same price offered to competitors.

The core principle is: Retail Price – Wholesale Price ≥ Downstream Costs

If the difference between the retail and wholesale price is not enough to cover the dominant firm’s own downstream costs (e.g., marketing, billing, customer service), it suggests that an equally efficient competitor would not be able to operate profitably, and a margin squeeze is likely occurring.

The Norwegian Squeeze Case: Telenor

The Norwegian Communications Authority (Nkom) and the EFTA Surveillance Authority (ESA) have conducted several margin squeeze tests on Telenor, Norway’s dominant telecommunications provider.

A prominent case, which resulted in a significant fine for Telenor, centered on its pricing for residential mobile broadband services.

The investigation, which covered the period from 2008 to 2012, found that Telenor’s wholesale prices for network access were set so high that competitors who relied on this access could not viably offer mobile broadband services to their customers without incurring a loss.

- The Abusive Conduct: Telenor’s pricing made it impossible for rivals to compete, particularly in the fast-growing market for mobile data on large-screen devices like laptops and tablets.

- The Regulatory Action: The ESA found that Telenor’s actions constituted an abuse of its dominant position on the wholesale market and imposed a fine of approximately 112 million Euros. This decision was upheld by the EFTA Court in 2022.

- The Principle Confirmed: This case cemented the use of the EEO test in Norwegian and broader EEA competition law, confirming that it is appropriate to use the dominant firm’s own costs as the benchmark for a margin squeeze analysis.

LET’S TALK MVNO

If you have any questions, please fill out the form and a member of our team will get in touch with you. We are always open for talks on how we can add value to your MVNO.

The Three MVNO Models

Building a successful MVNO requires a clear plan in three different areas: MVNO Operational Models, MVNO Business Models, and MVNO Wholesale Models. Industry guides often mix these topics together, which can cause confusion. To succeed, you must treat them as separate parts of your business. This helps you align your technical tools, regulatory requirements, and commercial goals.

MVNO Operational Models

Focus: Technical control and infrastructure ownership

Examples: Reseller, Thin, Medium, Full MVNO

Strategic Goal: Defining operational independence and capability

MVNO Business Models

Focus: Market segment, audience, and value proposition

Examples: Fintech, Lifestyle, Ethnic, M2M/IoT, Retail/Brand

Strategic Goal: Capturing specific customer niches

MVNO Wholesale Models

Focus: Financial structure and cost calculation

Examples: Retail Minus, Cost Plus, Capacity-Based, Revenue Share

Strategic Goal: Managing margins and wholesale risk