Research Report: A National Telecom Wholesale Network

Research Report: A National Telecom Wholesale Network to enable competition in the Thai telecom market.

Exploring the potential of National Telecom (NT), partnering with a mobile virtual network aggregator and enabler (MVNA/MVNE), to launch a National Wholesale Network for mobile virtual network operators (MVNO).

This approach can foster competition, drive innovation, utilize existing infrastructure and ultimately benefit enterprises and consumers by providing them with more choices and innovative mobile services.

EXECUTIVE SUMMARY

The merger between True Corporation (TRUE) and Total Access Communication (DTAC) on March 1st, 2023 in Thailand has significantly reduced competition in the Thai telecommunications market, and raised concerns about price increases, service quality decline, and lack of consumer choice.

This report explores the benefits of strengthening the role of National Telecom Public Company Limited (NT), as a neutral player by allowing it to retain its spectrum and partner with a Mobile Virtual Network Aggregator (MVNA) and enabler (MVNE), to establish a National Wholesale Network (NWN), as a solution to enable competition into the market via Mobile Virtual Network Operators (MVNO).

This approach can foster competition, drive innovation, utilize existing infrastructure and ultimately benefit consumers and enterprises by providing them with more choices and innovative mobile services.

Current Landscape and Concerns in Thailand:

The TRUE-DTAC merger created a duopoly controlling approx. 97% and raising concerns about:

- Reduced competition: Less choice for consumers, higher prices and lower service quality.

- Limited innovation: Reduced incentive for the duopoly to invest in technologies and services.

- Stifling of MVNO growth: Difficulty for MVNOs to access network infrastructure at fair terms.

Proposed Solution: National Wholesale Network (NWN):

- Allow NT to retain its spectrum currently slated to be returned next year (2025).

- NT partners with an MVNA/MVNE to enable a National Wholesale Network accessible to MVNOs.

- MVNOs can then use the NWN and offer competitive and innovative mobile services.

Benefits:

- Increased competition through MVNOs providing greater choice and affordable services.

- Enhanced innovation: MVNOs are well-known for driving innovation in the telecom sector.

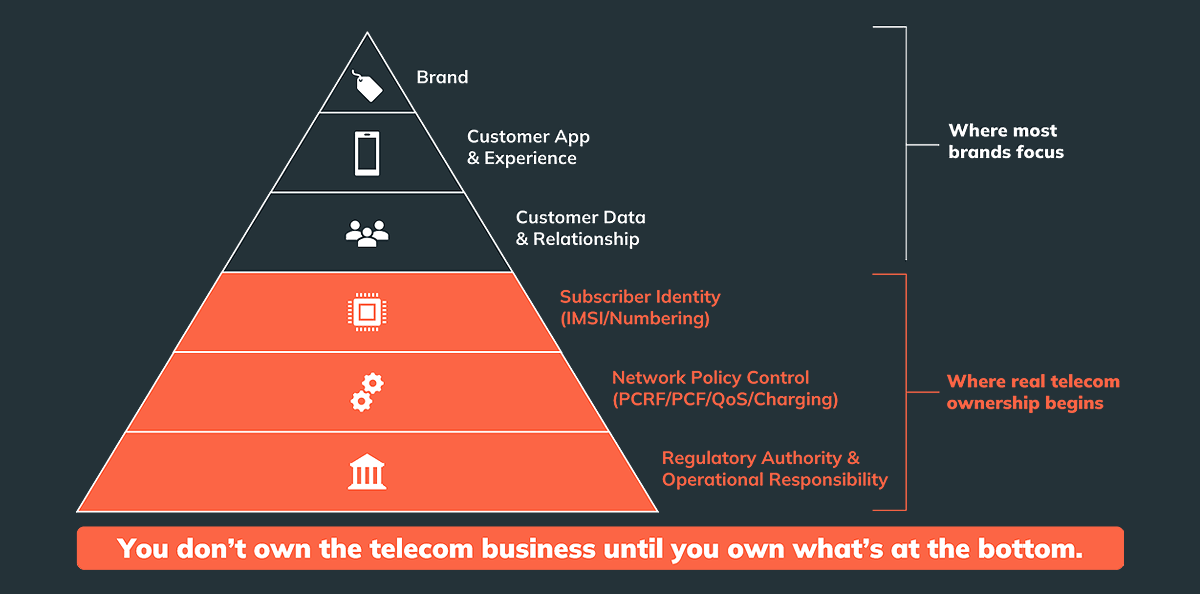

- Improved MVNO access: A neutral wholesale network would provide MVNOs with fair and transparent access to network infrastructure, fostering their growth.

- Promotion of Digital Inclusion: MVNOs often target specific niche markets or rural areas with tailored offers. A wholesale network could enable them to provide affordable mobile services to underserved populations, contributing to digital inclusion and closing the digital divide.

- Utilization of unused spectrum: Leveraging NT’s unused spectrum would improve spectrum efficiency and contribute to Thailand’s digital development goals.

Challenges and Considerations:

- Clear Regulatory Framework: ensuring fair competition and prevent anti-competitive practices.

- MVNA/MVNE: The right MVNA/MVNE partner is crucial. The ideal partner should be independent and possess strong expertise in MVNO operations and technology, along with a deep understanding of the Thai market. Effective collaboration and clear roles within the partnership is essential.

- Business Model Viability: Generating sufficient revenue from wholesale leasing to sustain the network and attract MVNOs will be crucial. Carefully considering pricing models, independence and trustworthiness and ensure sufficient demand from MVNOs are key factors for success.

- Network investment and operational costs: Maintaining a National Wholesale Network requires an efficient operation. NT has most of the infrastructure and spectrum in place already.

- Impact: The potential disruption to existing market dynamics needs consideration.

Conclusion:

Allowing NT to retain its spectrum and partner with an MVNA/MVNE to create a National Wholesale Network for MVNOs presents a strong solution to address the concerns arising from the duopoly.

This approach would foster a more competitive and innovative mobile market, benefiting consumers and contributing to Thailand’s digitalization goals. However, careful consideration of the implementation of a well-defined framework are crucial for successful execution.

Further Research:

- Detailed analysis of the potential economic impact of the proposed solution.

- Benchmarking with similar initiatives in other countries.

- Development of a regulatory framework.

Disclaimer:

This report does not constitute a comprehensive analysis of all potential benefits and implications.

1. MOBILE VIRTUAL NETWORK OPERATOR (MVNO)

1.1 Definition of MVNO

The industry and national regulatory authorities (NRA), have over the years adopted various local definitions for Mobile Virtual Network Operators (MVNO), but taking it word by word, provides a clearer understanding of the MVNO concept.

MOBILE – transportable, transferable, or movable. Relating to mobile cellular phones, handheld devices, and similar wireless technology.

VIRTUAL – almost, or nearly as described, but not completely.

NETWORK – connect as, or operate with a network.

OPERATOR – a person or company that engages in, or runs a business or enterprise.

Although there is no unified international standard on what precisely defines a MVNO, the International Telecommunication Union (ITU), defined MVNO as:

Based on a combination of the definitions from various national regulatory authorities and the ITU, an updated MVNO definition, look like this:

MVNO DEFINITION

1.2 MVNO Types & Operational Models

Beside the definition of Mobile Virtual Network Operator (MVNO) in itself, some national regulatory authorities have also adapted a range of sub-categories, or ”MVNO Types & Operational Models”, to further define and categorize the individual MVNOs.

These Types and Operational Models are largely defined by which of the operational components, network elements or facilities the MVNO manages and which one the host network operator manages, or the MVNE – indicating the depth of the individual MVNO’s market participation.

Based on this criterion, three main types of MVNO and operational models are observed: Thin, Medium and Full MVNO.

Note that the Full MVNO model is not available in Thailand.

Table: Operational Mode: Thin, Medium, Full MVNO and MVNE Architecture

| Functions | Sub-Function | Thin MVNO | Medium MVNO | Full MVNO | MVNE |

|---|---|---|---|---|---|

| Enabling infrastructure | Radio Access Network | MNO | MNO | MNO | MNO |

| Network Routing | MNO | MNO | MVNO owns | MVNE | |

| Content and Service | Value Added Services | MNO | MVNO may own | MVNO owns | MVNE |

| Applications & Services | MVNO may own | MVNO may own | MVNO owns | MVNE | |

| Operations | SIM Card / Number | MVNO may own | MVNO may own | MVNO owns | MVNO |

| Billing System | MVNO may own | MVNO owns | MVNO owns | MVNE | |

| CRM | MVNO may own | MVNO owns | MVNO owns | MVNE | |

| Marketing | MVNO owns | MVNO owns | MVNO owns | MVNE | |

| Branding and Sales | Sales & Distribution | MVNO owns | MVNO owns | MVNO owns | MVNO |

| Branding | MVNO owns | MVNO owns | MVNO owns | MVNO |

1.3 The MVNO Market

MVNOs are spreading across the globe, from the initial four MVNOs first launched in the UK and Denmark in year 1999/2000 to more than 2.000 MVNOs – in more than 90 countries, as of year 2023.

Illustration: There are now more than 2.000 MVNOs in more than 90 countries.

Europe continues to lead in terms of most MVNOs in operation with an estimated 1.016 MVNOs, representing half of the total global MVNO market. It is followed by:

- Americas with 386 MVNOs,

- Asia with 322,

- International: 132,

- Oceania: 86,

- Africa: 57,

- Middle East: 9.

In addition more countries are opening up for MVNOs. In example, Nigeria awarded 43 MVNO licenses to companies in Nigeria in 2023. The MVNOs are expected to launch in 2024.

The global MVNO market is projected to grow from USD 84.36 billion in 2023 to USD 149 billion by 2030, representing a compound annual growth rate (CAGR) of 8.5%.

APAC

The Asia pacific MVNO market was valued at USD 29.33 billion in 2021 and it is expected to reach a value of USD 46.42 billion by 2027, registering 7.93% CAGR.

Competition in the APAC MVNO markets has shifted from pricing to service and product differentiation while the telecom regulators across the region are leveraging MVNO growth to increase competition and the digital economy.

THAILAND

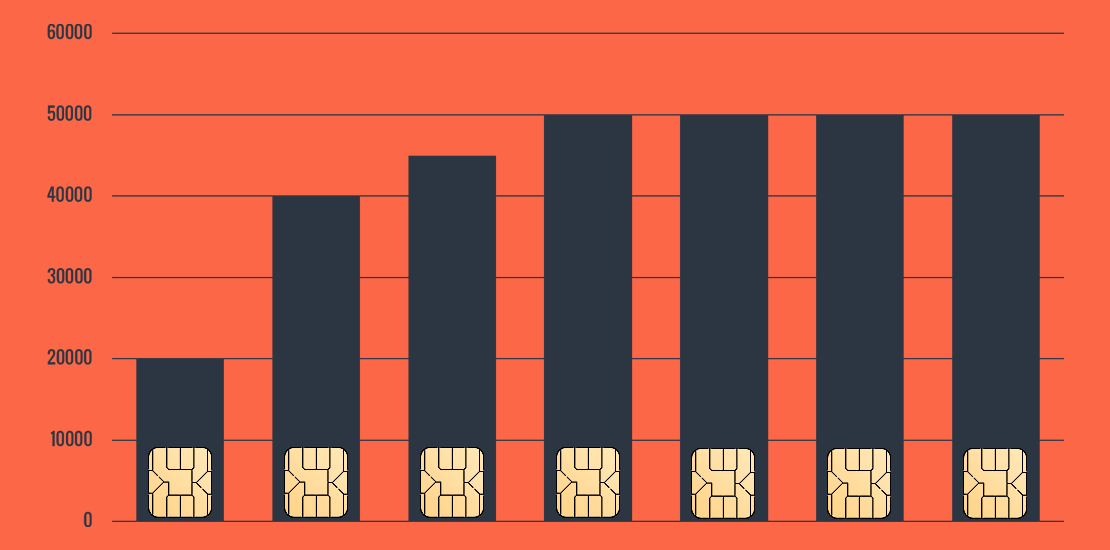

In Thailand, only 10 MVNOs have launched out of 60+ MVNO licenses awarded since the introduction of MVNOs in Thailand in 2009. Four of the ten MVNOs are active today with just about 30.000 active subscribers combined.

They are:

- iKool3G (Loxley),

- Penguin SIM (Whitespace)

- Feels (Feels Telecom)

- RedONE (From Malaysia).

Chart: The Thai mobile telecom service market EoY 2023.

1.4 MVNO Strategy: Market Differentiation and Segmentation

As mobile connections increase and the mobile penetration reach the saturation point, traditional mobile network operators (MNOs), find it increasingly challenging to compete and grow organically.

Competition shifts from being predominantly network based – where the MNOs compete on differences in network quality and coverage – to services based, where competition depend on the ability and flexibility to match service, price and features with specific consumer needs and wants.

A similar challenge happens when new generations of mobile network technologies are introduced into a market (3G, 4G, 5G). The MNOs are then (once again), competing against each other on network roll-out, while also trying to get their own existing subscribers to update to a new and more expensive package that delivers the same – only with more speed.

Mobile network operators suffer from the limitations of their traditional method of marketing – a “one-size-fits-all” strategy, where they approach all consumers, as having similar lifestyle, needs and demands, resulting in under-served and un-reached segments who does not feel they belong.

Market dissatisfaction comes from either poorly tailored products and services or intangibles, such as a mismatch between consumers individual lifestyles, and what their operator’s brands stand for.

Some Examples:

- Prepaid mobile customers feel like 2nd class citizens compared to the service offered to postpaid.

- The CFO of an enterprise doesn’t see the value of six months Netflix on the companies SIM cards.

- SMEs does not see the value on unlimited data on the SIMs they use for their calling center.

- Visually impaired persons does not see the value in the added Virtual Reality (VR) service.

- Different consumers simply do not all have identical needs – or identical use habits, which utilize the same operator value components all the time.

MOBILE OPERATORS are designed for distribution of mass market telecom connectivity services, however in the digital economy this logic shifts from the current supply focus, into a demand driven reality.

CONSUMERS in today’s digital economy require personalized, and innovative telecom services, but the mobile operators continue to deliver one-size fits all connectivity service and offers.

ENTERPRISES are increasingly demanding complete lifecycle services to support their digital business models and transformation, only to be met with standard offers of connectivity from the MNOs.

1.5 MVNOs Competitive Edge

Mobile Virtual Network Operators (MVNO) have utilized the above issues, achieved a competitive edge and captured market shares – by capitalizing on market differentiation and segmentation rather than merely competing on connectivity and price.

Instead of the view of customers as one large, indistinct segment – MVNOs embrace a targeted approach, creating a unique brand positioning and value proposition to attract a defined niche segment, such as specific groups or demographics and tailor their service, offer and products to the needs, value and lifestyle of this customer segment.

Deploying in this way ensures that customers’ needs are more accurately identified, and serviced. In return, customers respond positively, with growth resulting from the niche segment approach.

MVNOs can target a range of verticals and market segments by offering:

- Connectivity options that can be differentiated according to preference and context (i.e., differentiated data tariffs and connectivity for various sites, apps, location etc.).

- Platforms allowing the verticals/industry to control their own connectivity and business (Platform as a service, Software as a service, Connectivity as a service, Data Analytics, etc.)

- Differentiated non-network services such as customer care, bespoke services, brand and product characteristics, which create a sense of belonging according to lifestyle.

Fig: Mobile Network Operators(MNO) Marketing Strategy vs. MVNOs.

MNO – ONE SIZE FITS ALL

Mobile network operators suffer from the limitations of the traditional “one size fits all” marketing strategy – taking consumers as large averaged groups or as a few segments, resulting in underserved and un-reached segments.

Mobile operators realize that they can’t be all things – to all people and see the value of MVNO partners. Different consumers simply does not have the same needs.

MVNO – NICHE SEGMENTATION

MVNO’s cater to segments that are underserved or un-reached by the mobile operators. They create a unique brand positioning and value proposition to attract target niche clusters such as specific groups or demographics.

MVNOs serve those niche segments that the MNOs can’t reach by offering products and services customized specifically to the end-user lifestyles, needs and demand

1.6 MVNOs Leveraging on Existing Assets

Some MVNOs have made use of their existing assets including their existing customer base, brand affinity and distribution channels. They use these assets to create a unique brand positioning and value proposition in order to attract their target segment – using mobile service more as a transportation to sell their existing services.

One of the key competitive advantages of MVNOs is that they have a thorough knowledge of their segment, allowing them to cater to that segment in a far more personal, relevant way than MNOs can.

Table: MVNOs Leveraging on existing assets.

MVNOs play a key role in penetrating key underserved segments, such as youth, elderly, expatriates, low-income earners, SME’s, travellers, communities, etc. Segments that the MNOs struggle to adequately serve because such segments are typically too small for the MNO to justify tailored products and services.

The lean and agile business model of the MVNO, however, allows highly focused targeting resulting in benefits to the whole ecosystem: The MNO, the MVNO and the end-users.

2. MOBILE VIRTUAL NETWORK AGGREGATOR (MVNA)

Aggregate, comes from the Latin verb, “aggregāre“, which means, to add to – or collect into a mass or whole. An MVNA aggregates, a mass amount of data capacity (voice, text, data) from mobile operators, and resell it to MVNOs. In essence, an MVNA is a middleman, between the MNO and the MVNOs.

The entry of MVNAs to the ecosystem has help facilitate the entry of MVNOs by making the commercialization more efficient for both the MNOs and the MVNOs. The MVNA, is able to provide tailored offers that suit the needs and individual business models of each MVNO.

Even MVNOs that successfully combine internal resources and partnerships to navigate challenges and risks will still be disadvantaged to existing players due to lack of economies of scale. MVNOs need scale to negotiate favorable pricing terms on network leases with MNOs.

Buying on behalf of several MVNO clients, the MVNA obtains capacity access/data from the MNOs in large bulks, which in return provides the MVNOs with economies of scale benefits, similar to any other, manufacture-wholesale-retail ecosystem.

Another benefit for the MVNOs, is that the sharing of the business models and KPI’s are shared with the MVNA and not the MNO. This adds a level of security to the MVNOs, that the MNO will not copy and launch (before the MVNO) the services or promotion packages, that the MVNO intend to launch.

The MVNA itself, will have to harness the skills necessary to conceive and build customized offers for multiple MVNOs. MVNAs will need to transform MVNO visions into marketable, functional offers, featuring an attractive set of mobile products and services.

As eSIM spreads, there will be a growing demand for MVNA-type players who can negotiate agreements between different operators that provide automatic remote service when users cross borders.

An MVNA needs to have MVNO experience, posses strong analytical skills and market knowledge, in order to understand, support – but also question the MVNOs business models, subscriber and traffic forecast, as well as maintain ongoing MNO and MVNO managements.

For example, but not limited to:

- Identify the niche and value proposition,

- Customer Segmentation and needs,

- Product Portfolio,

- Tariffs, Bundles, Voucher, Fraud,

- Advertising and Promotions,

- Subscriber Analysis,

- New Product and Application Specification.

- Legal compliance,

- Definition of sales & payment channels,

- SIM Cards,

- Channel, and Distribution Management.

- Business Intelligence Reporting,

- Bundle and promotion offer development,

- Customer acquisitions & retention campaigns,

- Improvement of operational processes,

- ARPU, Churn management,

- Best time to market (launch services),

- Flexible and enhanced life cycle configuration.

MVNAs will need to play the vitally important partner role, guiding MVNOs’ marketing acquisition and channel development strategies. Many if not most potential MVNO candidates will not readily know how to apply existing marketing or distribution knowledge to wireless.

In its relationship with the MNO and MVNO, the MVNA needs to be flexible, agile and share the vision. It needs to make sure both parties achieve their goals, as the MVNA own success depends on this.

The MVNA will have to obtain flexible and competitive wholesale network agreements with the MNOs.

It may deploy certain elements, which allows it to execute functions for billing, monitoring and reporting, management of numbering resources, business intelligence, and other services that it requires to address the needs of multiple client MVNOs.

The MVNA can take these steps directly or enter into a partnership with a Mobile Virtual Network Enablers or (MVNE).

3. MOBILE VIRTUAL NETWORK ENABLER (MVNE)

Within the value chain, there are intermediary ICT companies between the mobile network operators and MVNOs, these are called Mobile Virtual Network Enablers or MVNE.

MVNE differs significantly from the other MVNx models. An MVNE does not provide public telecom services. It has no contact to the end-users and is therefore not subject to telecom regulation.

In the event that an MVNE would become interested in providing services to end users as a MVNO, they would be subject to regulation, as a MVNO.

MVNEs are intermediaries between the mobile network operator (or MVNA) and the MVNOs, they provide a platform with technical solutions and business infrastructure services that help to execute the launch and operation of MVNOs.

These services may include core network and infrastructure elements, billing, administration, operations, business support systems, operations support systems, analytics and provision of technological and network elements, among others – for the adequate provision of the service.

Prospective MVNOs often have little relevant experience to guide them through the different steps of the wireless service delivery chain and need to overcome many challenges.

High peak funding, lack of telecom skills and expertise, lack of economies of scale, limited technological and architectural knowledge of the MNO/MVNO ecosystem and operational complexity are among the major barriers to entry faced by potential MVNOs.

While the challenges for the mobile operators include the workload of administering the heavy processes associated with the launch and day-to-day operations of each individual MVNO.

The MVNE solves these issues.

MVNO KEY ENTRY BARRIERS

High Initial Investment

The procurement and integration of IT infrastructure requires a high initial the investment.

Lack of Telco Knowledge

Many companies, with a strong brand and a large customer base, qualify as MVNO candidates but are not attracted to the business due to lack of Telco/MVNO knowledge

Operational Complexity

Starting an MVNO business is faced with significant operational challenges ranging from using a new unfamiliar billing platform to customer service, managing SIMs, devices, analytics, etc.

The MVNE mitigates the barriers to entry for the MVNOs, and eliminate many of the integration issues that could otherwise slow deployment, or even sink the MVNO/MNO business in a market altogether

Table: MVNO and MNO pain points mitigated with MVNE.

| MVNO | MNO |

|---|---|

| The MVNE becomes the MVNO partner—not the MNO. Providing each MVNO access to create and manage its own service. | The MNO saves on infrastructure, subscriber acquisition costs, and workload with no risks, while gaining network market share and revenue. |

| Having the MVNE gives the MVNOs the opportunity to do what they do best, concentrate on customer acquisition, and outsource the rest. | The MNO receives revenue without having to deal with the administrative processes of launch and day-to-day operations of each MVNO. |

| As the MVNE will host multiple MVNOs, it is possible to achieve economies of scale, and thereby lower rates and greater margins. | Sustainability: Utilize and profit from selling wasted network and capacity resources. |

| MVNOs can get guidance from the MVNE’s dedicated team of experts, experienced in the launch and operation of MVNO services. | Address specific/niche segments through the MVNE’s mix of MVNO clients, and gain healthy and sustainable MVNOs. |

| The MVNE reduces the initial Capex and Opex, providing faster ROI because all agreements and the requisite infrastructure are in place. | The MVNE solution dramatically decreases the internal skill sets and time needed to launch an MVNO. |

The MVNO retains customer ownership and compensates the MVNE for the management of all layers of the wireless service delivery chain.

4. MVNO BENEFITS FOR MOBILE NETWORK OPERATORS

Onboarding MVNOs will allow the MNO to address specific market niches, which the MNO has not yet tapped into – incurring lower Subscriber Acquisition Costs (SAC) and add efficiency to the value chain by creating offers aligned to the needs of each of the existing segments.

Illustration: MNO Market Approach vs. Market Segment Approach with MVNOs.

4.1 Financial Benefits From MVNA/MVNE/MVNO Collaboration

Besides being a source of growth, MVNOs are creating a significant advantages for the MNOs in terms of improving its business profitability.

- With an MVNA/MVNE/MVNO partner, the Subscriber Acquisition Cost (SAC) for an MNO is zero, as the Subscriber Acquisition Cost is transferred to the MVNO.

- The Average Revenue per User (ARPU) for the MNO, is only slightly lower with MVNA/MVNO than the retail ARPU for the MNO without MVNO.

- The EBITDA margin percentage of the wholesale business, is much higher than that of the retail one for MNOs without MVNOs.

Illustration: MVNO creating advantages for the MNO in terms of business profitability.

For the MNO, the EBITDA margins for customers acquired by MVNOs is 3 times the margin from retail.

MVNOs help MNOs to drastically improve their EBITDA margins by reducing Subscriber Acquisition Cost (SAC) costs with only a slight reduction in Average Revenue per User (ARPU).

Network operators are continuously investing heavily into spectrum licenses and infrastructure to keep up with demand and new technology. These new investments are resulting in capacity which needs to be fully utilized – as much – and as soon as possible.

A MVNO partner strategy can fill this gap and generate economies of scale for better network utilization.

In the very beginning, MNOs opposed the entry of MVNOs by refusing the network access or making the market entry difficult by other means. In response MVNOs requested regulatory actions in order to open MNOs’ network. Since then, the MNOs attitude has changed and MVNOs are considered entities, not only to increase competition but also to increase benefits to the MNOs.

4.2 From a Single Brand MNO to a MVNO Multi-brand/Segmentation Strategy

The multi-segment, multi-brand approach is not new, but built on experience from other industries such as the automotive industry.

Today, the automotive market is heavily segmented and most car manufacturers actually own multiple automotive bands, each focused on a specific market segment with the product tailored for the unique needs of that segment.

Illustration: Shifting from a single brand to a multi-brand, multi-segmentation strategy.

4.3 MNO/MVNA/MVNE/MVNO Benefit Conclusion

Onboarding MVNOs will allow the MNO to address specific market niches, which the MNO has not yet tapped into – incurring lower Subscriber Acquisition Costs (SAC) and add efficiency to the value chain by creating offers aligned to the needs of each of the existing segments.

A MVNO partnership brings the following benefits and opportunities for the mobile operator.

- Financial Benefits: New revenue streams Higher margins • Quicker return of investment • Reducing costs (increasing the EBITDA).

- Strategic Benefits: Niche segment tapping Use MVNOs in segments where the competitor is strong • Obtain greater share of the total market traffic • New distribution channels, reach new consumers in unserved/underserved market segments • Risk sharing.

- Operational Benefits: Network utilization Share business processes to increase overall performance.

- Marketing Benefits: Minimize churn Grow market • Cross-sell • More value, innovation and choice for the end-users • Saved retail costs can be used to increase customer retention.

4.4 MNO/MVNA/MVNE/MVNO Case Stories

Case 1: Tele2 Russia’s “MVNO Factory”

In May 2017, Russian Tele2 launched its “MVNO factory” strategy.

The strategy enabled Tele2 to host a range of MVNOs in various niches, and by mid-2017, it had six MVNOs operating, and contracts with eight more.

In 2018, MVNO subscribers in Russia grew to 3.2M with Tele2´s MVNO partners accounting for 1.75M of those.

At the end of 2019, Tele2 had 21 MVNOs on its “MVNO factory”, serving 3.75M subscribers out of 10M total MVNO subscribers in the market – increasing Tele2’s revenue from the “MVNO factory” 133% year on year.

End of year 2020, the MVNO factory had 4.8M subscribers – with a revenue increase of 55% YoY.

The goal is to occupy 15% of the total market in Russia by 2024

Case 2: Internet Initiative Japan (IIJ)

Internet Initiative Japan (IIJ), runs a MVNA and MVNE on the telecom operator NTT, catering services to MVNOs, IoT and M2M companies.

From 1Q 2017 to 3Q 2017, the MVNO subscribers going through IIJ´s MVNE was 744,000.

From 1Q 2018 – 3Q 2018, the subscribers grew by 254,560 to 998,892 providing IIJ with a service revenue of USD 96.3M up 37.8% YoY.

In 1Q 2Q19, the subscribers grew by 105,000 to reach a total of 1 million providing IIJ with a revenue of USD 115.1 million up 16.7% YoY.

FY2020, subscriptions through the MVNOs on IIJ’s MVNE platform was 1.1 million with a service revenue of USD 153 million.

Case 3: MVNA/MVNE Surf Telecom Brazil

In September 2015, EUTV S.A launched the company ”Surf Telecom” via the network of TIM Celular SA (TIM) to provide services as a MVNA/MVNE.

In February 2021, Brazil had a total of 82 licensed MVNOs with 36 of them enabled by Surf Telecom. Among the MVNOs are the Brazilian Post Office and several football teams.

As of March 2022, Surf Telecom and its 43 MVNO partners had a total of 937,190 subscribers.

Case 4: Cell C South Africa

In 2016, South African operator Cell C announced it had launched a MVNA and MVNE setup, which allowed them to launch MVNOs efficiently.

In its FY 2017 report, Cell C’s reported its MVNE/MVNO strategy had been a key contributor to the revenue growth, with MVNO wholesale revenue increasing by 79% to USD 52.8M YoY and MVNO customers reaching 1.5M.

In 2018 wholesale revenue was USD 47.12M and MVNO subscribers 1.68M.

In 2019 wholesale revenue reached USD 53.55M and MVNO subscribers 1.91M.

In its H1 2020 result Cell C announced an 18% increase in revenue to USD 22.6M from MVNE/MVNO, as an important part of its turnaround strategy.

In first half of 2021, wholesale subscribers through MVNE/MVNO reached 2M.

2023: South Africa has seen a swell in mobile virtual network operators (MVNOs). In addition, Cell C, the challenger mobile network operator (MNO) is no longer operating its own network and spectrum, instead it has become a full MVNO itself in 2023 with a MVNE partner enabling MVNOs.

With roughly 12.8 million subscribers, Cell C has gone from South Africa’s fourth-biggest MNO to the country’s largest MVNO.

Cell C was South Africa’s only MVNE for years and provided services to South Africa’s very first MVNO, Virgin Mobile. Since then the other operators have launched MVNA/MVNE/MVNO platforms as well.

5. THE ISSUES IN THAILAND

Since the introduction of a MVNOs in Thailand more than 60 companies have obtained MVNO licenses. Ten have launched but only four are operational and struggling due to the issues in the market.

|

|

|---|---|

|

Local and international enterprises are interested in investing and launching MVNO services but are held back by the problems in the market. Enterprises are aware of the need to transform digitally but several are not interested in having to rely on and having their business (data) going through AIS or TRUE/DTAC. |

NT’s survival depends on wholesale. It has underutilized capacity but not the necessary knowhow, flexibility, and platforms needed to attract and support MVNO partners. The merger of TRUE/DTAC has created a duopoly in the market with consumers and enterprises demanding more choices. |

5.1 From Concession to Licensing to Oligopoly to Duopoly

Prior to the first auction (2100 MHz), that took place in 2012, the mobile operators had build-transfer-operate (BTO) concessions with the two state telecom operators TOT and CAT Telecom (NT today). AIS was on TOT, while DTAC and TRUE was on CAT Telecom. The regulator, National Broadcasting and Telecommunication Commission (NBTC), was introduced about the same time.

Before the introduction of the licensing scheme, TRUE decided to enter into a network access agreement with its concessionaire, CAT Telecom to use CAT Telecom’s 850 MHz network to launch 3G services before AIS and DTAC. The setup was not in line with the telecom act and initially declared unlawful. However, after a handful of amendments, it was cleared and classified, as a MVNO setup.

The NBTC, not 100% knowledgeable about the MVNO concept, came up with its own notification and regulation regarding MVNO, which looked like something a bride should wear at her wedding = “Something old, something new, something borrowed, something blue”.

NBTC also added to the 2100 MHz license terms and conditions (and in every spectrum action since), that minimum 10 percent of the capacity should go to MVNOs.

In 2009, five companies applied and received MVNO licenses in Thailand and launched on the two state enterprise operators TOT/CAT. When the first five MVNO’s where given a license to operate, TOT, had only 548 base-stations ready in Bangkok. A year later just 1,000 base stations was ready for service.

TOT was supposed to install 5,200 base-stations during phase 1 and complete the project by 2012. However the project finished with only 5,320 base station in 2013 and never got to phase 2.

Despite this, the MVNO, and local handset brand “i-mobile”, managed to obtain 600,000 subscribers at its peak in 2014. However, in the years that followed, its mobile handset brand lost steam to the Chinese competitors, and the MVNO never managed to pivot and closed its MVNO business in June 2017.

Chart: MVNOs and Subscribers in Thailand 2013 – 2023.

TOT has since then teamed up with mobile operator AIS, on an agreement bringing TOTs 2100MHz network coverage nationwide with more than 20,000 base stations in total. TOT also had DTAC roll out 4G LTE TDD on TOT’s 2300MHz with about 21.000 base stations.

5.2 Failure to foster MVNO competition

Besides approving MVNOs into the market and awarding licenses, the regulator NBTC has not been proactive in supporting MVNOs in the market.

The Inspection and Evaluation Commission of the NBTC, also known as the “Superboard”, concluded in April 2015 that the NBTC had failed in fostering competition in the Thai telecom market and the promotion of MVNOs. The Superboard found that the NBTC should issue better regulations for mobile virtual network operators to support more of them in the industry, which would benefit consumers.

TOT and CAT telecom (NT today) has been the only mobile network operators hosting MVNOs in Thailand. Neither AIS, TRUE or DTAC has hosted any MVNOs on their networks, since the introduction of MVNOs in Thailand, despite NBTC’s Mobile Virtual Network Mobile Phone Service Notification B.E. 2013, the revised Announcement in 2020, as well as described in the terms and conditions in the operators spectrum licenses since 2013, stating that minimum 10% of their spectrum capacity has to go to MVNOs.

The big three’s self-interest has caused a collective outcome of resisting MVNOs on their networks, If not the result of a coordinated behavior between the operators, then by deciding individually that MVNO access should be prevented.

With the merger of CAT Telecom and TOT on January 2021, the option for mobile virtual network aggregators (MVNA), mobile virtual network enablers (MVNE) and MVNOs to obtain wholesale network access, went from two to one, impacting the ability of MVNOs to enter the market.

Opposite, AIS, TRUE/DTAC has themselves taken advantage of using MVNO licenses and models to launch their own sub-brands into the market based on MVNO i.e. AIS with GOMO by Singtel and Finnmobile (DTAC), as well as enter into network rental/barter agreements with CAT and TOT (now NT).

Illustration: TRUE’s network agreement on CAT Telecom’s (now NT) 850 MHz.

Illustration: AIS’ network agreement on TOT’s (now NT) 2100 MHz.

Illustration: DTAC’s (now TRUE) network agreement on TOT’s (now NT) 2300 MHz.

2300 MHz MVNO setup")

Opposite merger and acquisition conditions in most markets, the conditions for the merger of TRUE and DTAC, did not come with conditions on divesting any of their spectra. Instead they got to keep the spectrum from both DTAC and TRUE, as well as the rental/barter agreements on NT’s spectrum.

Table: Mobile spectrum in Thailand pre the TRUE/DTAC merger.

Table: Mobile spectrum in Thailand post the TRUE/DTAC merger.

In addition, AIS has recently entered into a new rental/barter deal with NT for half of NT’s 700 MHz, leaving NT with just 5 MHz on the 700 MHz spectrum (to be rolled out).

As NT has to return is spectrum on 850 MHz, 2100 MHz and 2300 MHz next year (2025), they will only be left with 5 MHz bandwidth on the 700 MHz spectrum and 400 MHz on the 26 GHz band.

5.3 AIS and TRUE de facto controlling NT’s network and wholesale price

The wholesale network rental/barter agreements has placed the big three, not only in control of NT’s network capacity but also the wholesale pricing NT is able to offer to MVNOs.

As such, AIS, TRUE/DTAC are de facto in full control, of who can enter the market, by raising artificial barriers to entry, protecting their own retail business through high wholesale access fees, adversely impacting the ability of MVNOs to compete effectively at the retail level.

In example, when a MVNA or MVNO contacts NT today to discuss a wholesale agreement, NT has to inform AIS (2100 MHz) and TRUE/DTAC (850/2300 MHz) of this, and the two will provide a wholesale price to NT. However, as NT also have to make a business on this, it has to add its margin on top of the wholesale price they got from AIS/TRUE.

Furthermore, in order for AIS and TRUE to give NT a wholesale price to NT’s MVNO partners, AIS and TRUE say they need information from NT on the MVNOs, i.e. expected subscriber growth, capacity needs, type of plans, segment(s), etc. Hence AIS and TRUE are not only de facto controlling the wholesale price NT can give to MVNOs – they are also fed with information about possible competition.

AIS and TRUE/DTAC are thereby in control of the market at all times, and the MVNOs will always end up with a higher wholesale price, as they have to pay not only NT but also the two gatekeepers (AIS and TRUE) and those costs can only be forwarded to the end-users = no competition.

The competitive pressure the MVNOs have been able to exercise in Thailand has been extremely limited and was reduced to zero as a result of the TRUE/DTAC merger. Not only due to a further reduction in the number of wholesale network access operators, but also the decreased bargaining power of MVNOs in the negotiating process that follows. This applies both to prospective MVNA/MVNO entrants and to the existing MVNOs, once they need to re-negotiate their wholesale agreement – or switch host.

When CAT Telecom (now part of the NT) and True renewed their network/barter agreement, it was added in the agreement that only CAT Telecom’s own retail service (MyCAT), would be given access to 4G, thereby actively excluding MVNOs to use 4G on the network NT has access to on True.

Besides humans, and the rise of devices that needs connection and a tailored service and package with it, are in the millions. The mobile network operators cannot handle this by themselves. As seen in other markets, MVNOs are the perfect partner for such, as they are more agile.

5.4 Gatekeepers of the digital economy

The current MVNO setup in Thailand has zero chance to provide innovation and competition in the market. The operators have built barriers to entry by not having any active MVNA/MVNOs on their networks, opposite in other countries where MVNOs have accelerated in IoT/M2M, Ai, Blockchain, Fintech, new pricing and promotion models to both end-users, enterprises and government projects.

Thailand’s investment, support and effort to get 5G up and running successfully, is hampered by the lack of MVNOs being able to utilize it for the requested innovative services and support in getting various verticals and projects transformed into the digital economy. All the eggs have been placed in only two baskets or gatekeepers = AIS and TRUE/DTAC.

Lack of network access (or a MVNA partner) – and the lack of a suitable wholesale pricing regulation, are two of the key obstacles for the successful launch and operations of MVNOs.

Businesses who are in the same verticals, as some of AIS or TRUE’s sister companies don’t want to see their company or user data, having to pass through AIS or TRUE.

In example, Electric Vehicle (EV) companies, struggles to choose between an operator who’s shareholder is active in fossil fuel (AIS and Gulf Group) – or a operator who’s shareholder owns a competing EV brand (TRUE and MG). Similarly, Telehealth projects in Thailand should not use – and have patients data running through the two mobile operators who is also active in selling insurances.

The only other option these businesses and projects have, is to launch their own MVNO (or Private Network) to be in control of the data and own business. However, as no MVNA or MVNE partners are attached to any of the mobile network operators today, the MVNOs aren’t able to use the data they generate and run their own business, thus being pushed to use the “competitors” (AIS/TRUE)

The MVNOs that are operating in Thailand today are not even able to monitor and analyze their own generated business data, to see what part of their business and service is working or not.

For MVNOs, the lack of wholesale network access (or a MVNA partner attached to a mobile operator) – and the lack of a suitable MVNO enabler platform, are two of the key obstacles for the successful launch and operations of MVNOs.

The availability of a MVNA/MVNE in Thailand would not only lower the upfront capital cost for MVNOs by taking advantage of economies of scale (buying power) but also provide them with the necessary platform to launch and operate their own business – like any other businesses in Thailand are able to do.

It would encourage the businesses, who have already applied, approved and paid for a MVNO license in Thailand (but haven’t launched) – as well as the potential local and international MVNO candidates, who so far have steered clear of investing in Thailand due to the issues mentioned.

5.5 National Telecom’s (NT) 700 MHz

NT hasn’t been able to come up with a sustainable business plan and roll out its 700MHz 4G and 5G network, several years after it won the spectrum at the auctions in 2020. The only “solution” has been for NT to be dependent on AIS again.

Additionally, NT has to give back its existing 850MHz, 2100MHz and 2300MHz spectrum to NBTC next year (2025) and has already started to the existing MVNOs that they need to find other options.

“NT has no time to hesitate, needing to quickly complete its business turnaround as well as improve operating efficiency” NT’s board Chair Nattapon Nattasomboon told Bangkok Post.

This, raises a serious question: What will happen to MVNA/MVNOs in Thailand?

Because why would any company consider investing into a MVNO/IoT/M2M/Private network with only a few months horizon on their business plan/break-even/return of investment?

Although NT (or rather AIS) has started to roll-out a 4G/5G network on the 700 MHz, this is far from enough to support AIS, NT’s own retail service, MVNOs and Private Networks.

NT has about 2 million customers itself, and with AIS and NT taking up the capacity there is only space left for about 400,000 MVNO subscribers, which is not even enough for one MVNO to reach financial break-even on its investment in the Thai market.

In the deal between AIS and NT, AIS will be operating NT’s capacity and NT will rent and pay rental fees to AIS’s network, and related equipment that NT will use to provide its own service on the remaining 5MHz of the spectrum, which will be both 4G and 5G.

As the operation of the 700 MHz will be under AIS, NT will have to pay rental fees to AIS, which will further increase the wholesale price NT can offer to the MVNOs. Hence the MVNOs will never be able to compete. In addition, AIS will need to get information from the MVNO’s business, in order to manage the capacity for them. As such, AIS will have the unfair advantage of knowing what the possible competition is up to and take action before it arrives.

With the 700 MHz, the MVNOs will also be burdened with the heavy costs of changing all their SIM cards (SIM swap), as their customers would need to be moved from the existing 2100 MHz and 2300 MHz spectrum to the 700 MHz. This will result in further loss of customers in addition to the large cost and time related to make and distribute new SIM cards.

The main problems in the Thai mobile market boils down to three major issues:

- Lack of network access,

- Lack of MVNA/MVNE/MVNO expertise,

- Lack of the necessary technology platform

5.6 Single Points of Failure

On May 10, 2024 at around 16:00 o’clock, customers of AIS – one of Thailand’s only two mobile network operators – found themselves unable to use mobile data with their mobile phones showing the “No Service” symbol.

Dr. Saran Boonbaichaiphruek, Chair of the telecom regulator NBTC, called a urgent meeting with the executives of the Office of the National Broadcasting and Telecommunications Commission (NBTC Office) after the AIS outage, as well as ordering AIS to explain the cause of the incident.

“AIS must explain the cause of the incident, because a large number of people were affected, unable to make calls or use the internet for unknown reasons. I myself has been affected as well. A penalty may need to be considered in order to make the signaling maintenance more efficient”, said the NBTC Chair.

The AIS outage, highlights that having only two mobile networks as gatekeepers in Thailand leads to severe vulnerabilities and challenges during outages or disruptions.

After the merger of True Corporation and dtac last year, there are only two mobile network operators in the market; AIS and TRUE/DTAC.

As of Q1 2024, the duopoly is sitting on 98.74% of the total 97.3 million connections in Thailand.

- AIS has a market share of 46.27% = 45 million subscribers/connections.

- TRUE has 52.47% = 51 million subscribers/connections.

The state-enterprise National Telecom (NT), does have spectrum on the 850 MHz, 2100 MHz and 2300 MHz, for its own public mobile services and MVNOs, but the network on this spectrum is de facto operated by AIS and TRUE/DTAC. In addition, NT’s 850 MHz, 2100MHz, 2300 MHz is set to be returned next year for auctioning.

Relying solely on AIS and TRUE as the only two network providers in Thailand means that any significant issue, affecting either network (such as technical failures, natural disasters, or cyberattacks) will have widespread consequences and affect millions of users. Businesses, hospitals, emergency services, public services, law enforcement and other organizations across the country, will face disruptions.

Case in point: The outage at Australia’s telecom operator Optus (Singtel) in November 2023, which left 10 million Australians (40% of the population), without internet or phone services. The outage impacted business, payment, logistic and health systems and raised questions about the country’s core infrastructure.

6. SUPPORT FOR MVNA/MVNE/MVNO IN THAILAND

The Thai telecom sector has been far behind other markets in enabling policies and dealing with barriers to entry for new entries to the market, since the National Broadcasting and Telecommunication Commission (NBTC) was introduced in 2011, resulting in significant market power and control to the three operators (now only two).

The former leadership at the NBTC passed the buck of dealing with TRUE’s takeover of DTAC to the new (current) leadership, as its first job when they took office in 2022.

Since then, the NBTC board has been split into two groups with the NBTC office, as a third wheel with major delays in decision making, regulation and administration of the market as a result, causing frustration among end-users, consumer associations and politicians, who have/are actively and increasingly voicing their opinions and frustrations.

The complaints and comments have not just targeted the two operators, AIS and TRUE but also the NBTC for its failure, as a regulator to listen to, react and protect the consumers.

DISAGREEMENTS BUT ALL UNITED ON BOOSTING MVNO

Interestingly, although there is disagreement on how to tackle the issues of the merger, merger conditions, pricing and declined network quality – one thing they all seem to be united on – is the entry and promotion of MVNOs into the Thai market.

NBTC Board Commissionaire regarding Telecom Business

On October 20, 2023, NBTC Board Commissionaire regarding Telecom Business, Mr. Sompop Phuriwikraiphong said the important issue and policy for the NBTC, is to promote the creation of MVNOs. “But in the past, there has been problems from high cost of MVNOs purchasing access to spectrum or not getting any access at all from the private network operators. The NBTC therefore has to hasten to issue policies to encourage the launch of MVNOs, in order to create an alternative access to telecommunications services”.

The Senate’s Committee on ICT & Telecommunications

The Senate’s Committee on ICT & Telecommunications, appointed a sub-committee to investigate and help solve the problems at the national telecom regulator (NBTC), in November and in the press release that followed it revealed 7 agenda items, among them: Accelerate the push for mobile virtual network operators (MVNO) to create more competition in the market.

Thailand’s Consumer Council

On December 15, 2023, Thailand’s Consumer Council held the live online event “Talk 2 Action” where it called for a handful of policies including the introduction and promotion of MVNOs into the market.

The Move Forward Party

Five days later, December 20, Sirikanya Tansakul, MP from the Move Forward Party, gave their take on the need for MVNOs in Thailand in a interview on Channel 3’s “News Talk”.

The Chair of the NBTC

The support for MVNOs culminated when Dr. Saran Boonbaichaiphruek, Chair of the NBTC, revealed 9 urgent policies that will be accelerated in 2024, to increase and help facilitate options and services for the people in the country and break market dominance.

Among the 9 policies announced by the Chair of the NBTC are:

- The creation and promotion of a easy-to-connect MVNA/MVNE platform to enable and support MVNOs into the market.

- The acceleration and implementation of “One Region, One MVNO” with the goal of adding at least seven regional MVNOs in the market to increase options and services for the people.

- Reduce rates of the regional MVNOs by at least 20% from the plans of the duopoly.

- Out-of-area rates and interregional fees that suits the cost of living in that region.

- Conditions that makes sure the two large mobile network operators cannot own more than 25% of shares in a regional MVNO.

The Office of the National Economic and Social Development Council

In its report: “Conditions of Thai society in the fourth quarter and overall picture for 2023“, released on the 4th of March 2024, the Office of the National Economic and Social Development Council writes:

“There are issues that need to be followed up and given importance, namely; the impact of consumers after telecom mergers and acquisitions, that results in the price of monthly service fees for mobile service increasing, and some promotion packages have also reduced call minutes. Moreover, consumers are still experiencing problems with signal quality, especially the internet signal.

Therefore, the NBTC should review/add guidelines with clear supervision, such as setting a ceiling/controlling the price of the average service rate to be appropriate – as well as having measures to seriously promote new entrepreneurs into the market.”

Human Rights Commission Thailand

During its press conference on March 8, 2024, Commission member Supattra Nakaphiw from The National Human Rights Commission Thailand (NHRCT), issued a statement.

In the statement, the NHRCT points out NBTC’s decision to “acknowledge” the merger of TRUE and DTAC, will cause low-income groups in the provinces and remote areas to be left behind without telephone and internet services.

In addition, low-income people in urban areas must pay higher service fees. This may be considered a violation of the right to access basic public utility services.

NHRCT also mentions that the Thai Constitution 2017, Section 60, stipulates that the state must preserve spectrum frequencies and the right to access satellite orbits – that are national property – to be in the best interests of the people, state security and public benefits.

Therefore, in order to prevent human rights violations, and to ensure that business operations are in accordance with the UN Guiding Principles on Business and Human Rights (UNGP), which specify the duties of the government and the responsibilities of the business sector in respecting human rights – the NHRCT, at its meeting on “The Protection and Promotion of Human Rights“, on March 5, 2024, agreed that there should be recommendations to the NBTC, which can be summarized as follows:

- Prepare a road map to encourage the creation of mobile virtual network operators (MVNO).

- The NBTC should report results of the merger operation to the public, every 6 months until new operators come in and increase the competition in the market and bring down the high Herfindahl–Hirschman index (HHI) to normal level.

- Report, changes or impacts on consumers and the results of operations according to the specific merger conditions set by the NBTC, including the results of the NBTC’s actions, in the case merger is unable to implement the conditions.

- Expand internet service coverage to marginal or remote areas.

- Amend and improve the laws regarding measures to supervise M&As in telecommunication businesses and invite the Office of the Trade Competition Commission (TCC) to give opinions.

- Amend the method for calculating service rates to prevent promotional campaigns that take advantage of consumers and prevents people with low incomes from having equal access to the internet.

NBTC Public Hearing

The NBTC, held a public hearing (April 23, 2024), on the Telecommunications Master Plan No. 3 (2024-2028) draft, highlighting strategies to “promote competition via MVNOs, reduce digital inequality and protect consumers”

Although five strategies, was on the agenda for the public hearing, most of the participants at the hearing wants the NBTC to make a clear spectrum management plan (Spectrum Roadmap), and urged the NBTC to improve the ecosystem and framework for MVNOs to bring much needed competition into the market.

Captain Ativat Asvasirayothin, Chair and founder of the MVNO A Telecom Company Limited, suggested that the NBTC should enforce regulations and encourage the large operators to allow MVNOs on their networks with the NBTC setting the details on wholesale pricing.

Admiral Prasarn Sukkaset, Chair of the NBTC’s Performance Monitoring and Evaluation Committee said: “Last year, MVNOs declined significantly, as competition in the market was reduced by the True-Dtac merger. He asked for an increase in the market concentration index (HHI), which measures the level of competitiveness in the market”.

Representatives from the Office of the Trade Competition Commission (TCCT), joined in expressing their opinions regarding inequality, noting that inequality is not just in terms of access to telecommunications services. But there are also disparities between entrepreneurs. “The concern of the TCCT is on competitive pricing standards, because now the big operators can lower their prices but the smaller operators cannot, so the NBTC should create equality in competition.”

Public sector representatives who have worked in the telecommunications industry for more than 20 years also gave their opinion that spectrum frequency plans “need to be more detailed than they used to be, because there is a range of spectrum that is about to expire, and how many new ones will be auctioned?”

Atip Keeratipich, CEO of the MVNO Red One Network (Thailand) said: “We are dependent on NT who is gracious to us. But the 850 MHz, 2100 MHz and 2300 MHz bands held by NT will expire in September 2025. Therefore, we have an urgent need to see an Action Plan including the MVNO’s agenda, and additional time period from the NBTC, because we are not able to make a 5 year business plan. We hope the NBTC will accept and consider this“.

7. THE SOLUTION: A NATIONAL WHOLESALE NETWORK (NWN)

This report suggest taking advantage of the role of NT, as a neutral state-owned player, by allowing it to keep its current spectrum and infrastructure, and then partner with a MVNA/MVNE, to establish a National Wholesale Network (NWN) – a wholesale-only network offering 4G/5G access and telecom support to large and small enterprises, communities, government projects, etc. as MVNOs.

A National Wholesale Network (NWN) will drive innovation, utilize existing infrastructure and spectrum, benefit consumers and enterprises, providing them with choices and innovative services, establish effective competition at the retail level boosting the digital transformation and economy.

Illustration: National Wholesale Network (NWN) Thailand – Ecosystem.

- NT is responsible for the spectrum and the matching network infrastructure for the nationwide distribution of telecom services.

- A NBTC licensed MVNA buys wholesale access to the National Wholesale Network on behalf of MVNOs, using economies of scale to achieve a discount, and then resell the access to each MVNO.

- A MVNE provides each MVNO with an instance access to a platform with the telecom technology needed – such as data analyses, operations and business support systems – enabling the MVNOs to operate and customize their own service 24/7. In addition the MVNA/MVNE support the MVNOs through all aspects of the customer lifecycle, from launch to operation by adding, and fully capitalizing on their MVNO, local market and retail expertise.

- The MVNOs provide their own tailored services to the wants and needs of their own specific segments – be it people or machines – under their own control, brand and pricing.

Providing an all-in-one turnkey solution of expertise, connectivity and technology to enable a full range of service offers. In addition the MVNA/MVNE market experts can cooperate with NT for NT’s own retail service.

7.1 Benefits

- Increased competition through MVNOs providing greater choice and affordable services.

- Diversification by having more operators and networks will distribute the risk and reduce the impact of a single point of failure.

- Enhanced innovation: MVNOs are well-known for driving innovation in the telecom sector.

- Improved MVNO access: A neutral wholesale network would provide MVNOs with fair and transparent access to network infrastructure, fostering their growth.

- Promotion of Digital Inclusion: MVNOs often target specific niche markets or rural areas with tailored offers. A wholesale network could enable them to provide affordable mobile services to underserved populations, contributing to digital inclusion and closing the digital divide.

- Utilization of unused spectrum: Leveraging NT’s spectrum would improve spectrum efficiency and contribute to Thailand’s digital development goals.

- A neutral wholesale network and MVNA/MVNE: With no other commercial interest. Providing a safe haven for enterprise business and end-user data i.e. for Telehealth projects.

7.2 Benefitting all Stakeholders

A ecosystem build on a sustainable model generating value and therefore motivation to all stakeholders.

NATIONAL TELECOM (NT) will be able to fully utilize existing infrastructure and wasted spectrum capacity while adding a new wholesale revenue stream to its books.

THE MVNA/MVNE benefits from being a part of the digital economy and revenue the more successful the MVNOs are.

MVNOs benefits from getting network access and having a MVNA/MVNE partner, who is supporting the MVNOs in becoming successful, as the MVNA/MVNEs business depends on the success of the MVNOs.

ENTERPRISES will have access to build and operate their own mobile services as MVNOs and use the data it produces to support their digital transformation and business models.

CONSUMERS benefits from competition on innovative services and cost effective prices customized to their lifestyle, as competition will now be focused on services rather than network technology.

THAILAND benefits from the increase in users/usage in the digital economy – stimulating economic growth. New revenue stream from a state-enterprise. Sustainable usage of infrastructure and spectrum, as well as new jobs and skills development in the digital economy.

7.3 Challenges and Considerations

Spectrum Allocation – Stare decisis

Although Section 45 of the Frequency Allocation Act stipulates that spectra must be allocated through auctions and that after expiry of concessions, spectra must be returned to the NBTC for reallocation, there is also precedent for allocating spectrum by other means than by auction.

a) In 2014, NBTC made a deal with TOT (now NT), where TOT got the permission (no auction) to use the 2300MHz in return for giving up its 900MHz, so the NBTC could hold a 900MHz auction. It is the same spectrum we are talking about today (2300MHz).

b) The Thai Constitution, Section 60, stipulates that the state must preserve spectrum frequencies – to be in the best interests of the people, state security and public benefits.

Section 60. The State shall maintain the frequencies and the right to access a satellite orbit, which are national treasures, in order to utilize them for the benefit of the country and the people. The arrangement for utilization of the frequencies under paragraph one, regardless of whether it is for radio broadcasting, television broadcasting and telecommunications or for any other purposes, shall be for the greatest benefit of the people, security of the State, and public interest as well as the participation of the people in the utilization of frequency, as provided by law.

c) In July 2024, the NBTC board unanimously gave its approval for the sale of the rights to use the two orbital slots via a combination of two methods: an open direct award and a beauty contest.

d) August 27, 2024, NBTC Commissioner, Dr. Thanapan Haraijaroen chaired a public hearing on the criteria for the FM radio frequency auction. Dr. Thanapan said that the criteria for the auction are in accordance with Section 41 of the Frequency Allocation Act. However, for community and public radios, it will be carried out by the selection method (Beauty contest), which has already been conducted.

e) October 20, 2024, NBTC commissionaire for telecom, Sompop Phuriwikraipong, reveals that the NBTC board meeting voted 5:2 in favor of allowing TC Space Connect Co. , Ltd., a subsidiary of Thaicom Public Company Limited, to receive the right to use a fixed satellite at the position of 50.5 degrees East, offering the government a return of 0.25% of the revenue per year.

f) There has been discussions and reports, on allocating spectrum by other means than by auction since 2014, following the first auction in Thailand, as the primary barrier to successful auctions is the low number of qualified bidders in Thailand.

g) A set of amendments was added to the National Broadcasting and Telecommunications Commission Act, in late 2021. A royal decree that ”supports convergence of technologies for the benefit of the country,” was formulated based on Section 30 of the amended Act.

h) NBTC received recommendations from the House of Representatives and the Senate to add the definition of “technology convergence” stipulated in the legislation, as the infusion of technologies for the benefit of the country, people and economy. Along with it, the NBTC also drafted four new regulations:

- Criteria for allocating spectrum ranges other than from auctions,

- An amendment to the Spectrum Management Master Plan,

- Criteria for applying for business licenses,

- Criteria for spectrum license transfer.

i) Paragraph two of “Authority of the NBTC” says: “To allocate frequency assignment between frequencies used in Television Business, Radio Communications Business, and Telecommunications Business” – It does NOT say “auction” but says “allocate” and “assignment”

A spectrum auction will not bring the best value

AIS and TRUE will probably challenge a decision to let NT keep its spectrum, with the help from GSMA (the lobby organization of mobile network operators), citing the need for the spectrum to be auctioned instead for “economical benefits” and the “digital economy”.

However, the regulator must consider the situation in the market = will an auction bring the best value?

a) The market is de-facto a duopoly with only two operators AIS and TRUE/DTAC making the amount of bidders even lower than in 2013, where it was already low.

b) The only other time, another party entered a mobile spectrum auction in Thailand was when JAS Mobile Broadband, a subsidiary of Jasmine International, entered the auction for the two 900 MHz licenses in 2014. However, Jasmine was unable to secure sufficient financing and bank guarantees in the market.

Subsequently, AWN (AIS) “won” the re-auction with no other bidders.

10 years later (2024), the NBTC approved AIS’ 100% acquisition of 3BB, as well as a 19% stake in Jasmine Broadband Internet Infrastructure Fund (JASIF), the owner of 3BB’s fiber optic assets.

c) After the TRUE/DTAC merger, the mobile packages by AIS and TRUE/DTAC somehow came up with the same pricing and usage amount. If not the result of a coordinated behavior between the two, then by deciding individually on the packages and pricing, which somehow magically caused a collective outcome. Could a similar magic collective outcome happen at an auction?

d) AIS and TRUE sent similar worded letters to the NBTC about the need for a reprieve on their 900MHz auction payment, which was granted by adding another 5 year instalment period and an interest rate of only 1.5% for the extension period. The controversial extension meant that around THB 19 billion – supposed to benefit the public went to the two operators. This underlines the issue with the auction approach.

e) Opposite other merger cases, the NBTC did not add spectrum divestment, as part of its TRUE/DTAC merger conditions. Instead, the merged entity maintained and combined TRUE’s and DTAC’s individual spectrum holdings, thereby changing the distribution of spectrum in the market.

f) More than a year has passed, and TRUE/DTAC has not delivered on the merger conditions, without any consequences, and as such NBTC could consider not allowing TRUE/DTAC to participate in an auction.

g) Since the first license was awarded in 2013, and all licenses since, it states in the terms and condition of the licenses, that a minimum of 10% of the capacity has to go to MVNOs. AIS, TRUE and DTAC has never delivered on these terms. The MVNA and MVNOs have never gotten their capacity – only from TOT and CAT Telecom (NT today).

h) NBTC is considering defining a portion of the 3500MHz for private networks. NBTC commissioner Somphop Purivigraipong, who is responsible for telecom business, said that the allocation should not be carried out via an auction. The high cost for spectrum investment would create a barrier to promoting a 5G private network, he said. However, he also said that the NBTC is unable to prohibit AIS and TRUE/DTAC from participating in the allocation process, even if this portion is mainly supposed to be for an industry 5G private networks.

NBTC commissionaire Somphop Purivigraipong’s decision to auction NT mobile spectrum will further solidify AIS and TRUE’s duopoly in the Thai Telecom market, leading to market failure with no competition.

Post such an auction, it is expected that TRUE will sit on 52 percent of the consumer-based mobile spectrum, AIS will have 47 percent, leaving only 1 percent to NT and its MVNOs. The Spectrum NT has left can maximum accommodate 2M users = Market failure!

As such, the spectrum auction suggested from NBTC would be unable to perform to the best advantage.

7.4 Modeled on Best Practice

The suggestion of a National Wholesale Network (NWN) in Thailand, is largely modeled on best practice from MVNA/MVNEs and the Single Wholesale Networks (SWN) in:

Mexico: Red Compartida (Shared network), is a national, independent wholesale 4G-LTE network and the result of the Mexican Government’s effort to overhaul its telecommunications industry by introducing competition into the marketplace. See more on the Red Compartida below.

Malaysia: Digital Nasional Berhad (DNB), is a Malaysian special-purpose vehicle company owned by the Ministry of Finance Malaysia. DNB was established in March 2021 to promote service-based competition in Malaysia and drive the development of 5G.

In 2021, Malaysia created a Single Wholesale Network (SWN) model, through the formation of the government owned Digital Nasional Berhad (DNB), to manage the infrastructure. This allowed all service providers in Malaysia to join the network through wholesale access agreements. As a result, all the major players have successfully launched 5G services.

DNB was established to accelerate the deployment of 5G infrastructure and network in Malaysia, and realize its potential to spur Malaysia’s Digital Economy and future, in line with the goals of the Malaysia Digital Economy Blueprint (MyDIGITAL).

Prior to DNB, the private sector telcos took six years to achieve a 80% 4G coverage, often prioritizing urban areas due to cost considerations. This resulted in a digital divide, leaving rural areas underserved.

Thanks to DNB, Malaysia leapfrogged most of its Asean peers in 5G and propelled Malaysia to the forefront of 5G adoption in ASEAN. Malaysians now benefit from faster, more affordable high-speed data.

In its latest research article (March 17, 2024), the mobile network testing, data and analysis company, Ookla commended Malaysia’s 5G network for its overall performance and consistency, noting how the network continues to lead, not only outperforming its Southeast Asian neighbors on 5G performance, with a 5G median download speed of 451.79 Mbps, higher than Singapore’s 329.73 Mbps, Thailand’s 129.40 Mbps, and the Philippines’ 125.14 Mbps – but also globally in terms of consistency, where it scored the highest Consistency Score globally for Q4 2023 at 97.3%.

At the end of 2023, DNB’s 5G wholesale network had achieved a 5G adoption rate of more than 30% and reached a 80.2% coverage in populated areas. In comparison, Thailand launched 5G in 2020 and at the end of 2023 the 5G adoption rate in Thailand was only 20%

It is important to underline that DNB is not a monopoly — it is an agnostic wholesale operator that provides equal access – on equal terms – to all operators, creating a competitive free market environment to the benefit of all consumers and enterprises.

The is clearly seen in the wholesale pricing from DNB where 5G from DNB’s network is 76% cheaper than the wholesale price on 4G from the network operators 4G networks.

The average wholesale pricing for 1GB data on DNB’s 5G is RM 0.12 per GB, versus the average 4G pricing on the operators networks which is RM 0.50 per GB.

RM 0.50 = THB 3.85 (USD 0.11) per GB (4G), and RM 0.13 = THB 0.92 (USD 0.02) per GB (5G).

In comparison the price per GB in Thailand is THB 92.16

Chart: Average Wholesale Price 4G and DNB’s 5G in Malaysia.

The wholesale pricing from DNB means that the mobile network operators (MNO) and mobile virtual network operators (MVNO), can offer lower prices on 5G than 4G. In addition they are now competing on services and innovation rather than pricing and spectrum/MHz.

Chart: Average Retail Price 4G and DNB’s 5G in Malaysia.

Had the Malaysian Government decided to stick with the success plan of DNB and not to open for another network, DNB would become cash flow positive in 2025, with an estimated IRR of >8% and worth RM16 billion to RM20 billion.

DNB’s successful deployment of a national 5G wholesale network was instrumental in attracting over RM160 billion of digital investments into the country, transforming Malaysia into one of the fastest-growing data center hubs in the world.

The wholesale network has spurred advancements across the entire ecosystem, including last-mile connectivity, solutions, and innovative use cases, ensuring Malaysia’s global competitiveness, ultimately benefiting the country’s economy and currency.

Brunei: Unified National Networks (UNN), an organization 100% wholly owned the government of Brunei Darussalam. UNN’s purpose is serving Brunei’s digital telecommunication, offering 3G, 4G, 5G wholesale telecommunication services to both national and international clients.

However, opposite these Single Wholesale Networks (SWN) projects, Thailand’s National Wholesale Network (NWN), has the advantage of less investment in spectrum and infrastructure, as NT has existing infrastructure and spectrum. In addition, NT is already used to other operators renting access.

7.5 Case Story: Mexico Red Compartida

More than just another mobile phone network — Red Compartida it is seen as a part of national infrastructure that is vital to the nation’s economic and social development.

América Móvil, the company owned by Carlos Slim, the world’s richest person between 2010 and 2013 had long held a monopoly in the telecom sector in Mexico with consumers complaining on “high costs and spotty service”.

Faced with a non-competitive telecommunications sector, Mexico’s telecommunications sector underwent a major reform to address the lack of competition and encourage investment and in 2015, the government announced the “Red Compartida” initiative.

To ensure true independent competition, a national, independent wholesale network named “Red Compartida” (Shared Network in English) was to be rolled-out with the aim of creating a nationwide 4G-LTE network as a vehicle for MVNOs to enter the market, increase innovation and consumer choice, improving quality of service and, ultimately, overcome the digital divide between urban and rural areas.

Initially, the project was setup as a Public Private Partnership (PPP) with the company Altán Redes that won the domestic and international public tender process.

The Red Compartida network is “wholesale only”, meaning that Altán Redes the company who build and operates the network would not be providing mobile service to end-users. Instead, the operator provides access to the network to MVNOs, who use the network to provide their mobile services.

In 2017 the government handed over the 90 MHz bandwidth on the 700 MHz spectrum frequency to the Red Compartida project and Altán Redes began the roll-out of the network in 2018.

However, rolling out a entirely new network infrastructure, especially to sparsely populated rural areas comes at a high cost and returns on investment takes longer, and in July 2021 Altán Redes filed for bankruptcy aiming to use protection to renegotiate its debts.

In June 2022 the government signed an agreement to become the majority stakeholder in Altán Redes and the company emerged from bankruptcy. At the time, Red Compartida had achieved a roll-out coverage of 70% of the population.

As with similar projects, GSMA, the lobby organization of mobile network operators was not late to criticize and call the project a failure – however the results speak for itself.

As of January 2024, the network coverage is 92.2% (103,5 million of the population).

At least 53 MVNOs launched and began operations in 2021 and 2022, and at the end of 2022 a total of 111 MVNOs were operating in Mexico.

In an interview with El Financiero, on March 13, 2024, Carlos Gabriel Lerma Cotera, General Director of Altán Redes, explained that 2023 was one of the best years for the National Wholesale Network, which doubled its number of users going through the platform via wholesale and MVNO partners – going from 5.5 million to more than 11 million.

The General Director also noted that the company will begin to focus on 5G Private Network service to the industrial sector as well.

Chart: MVNOs launched in Mexico in the period 2014 – 2022.

The mobile subscribers and connections served by the MVNO in Mexico quadrupled from 2020 to 2022, going from 2.55 million to 10.52 million representing a market share growth from 2.5% to 8.6% of total mobile connection in the country.

The telecom regulatory authority, Instituto Federal de Telecomunicaciones (IFT) estimated that the figure has risen to 13.3 million at the end of 2023, equal to a market share of 9.7% of total connections and equivalent to an increase of 2.5 million mobile subscribers/connections in one year.

Chart: MVNO connection/subscriber development in Mexico 2014 – 2023.

Of the 111 MVNOs operating in Mexico 61% of them were doing so only via Red Compartida. 22% via one of the traditional operators (Telefónica, Telcel, AT&T), and the remaining 17% using both a traditional operator and Red Compartida.

From 2020 to 2023, the MVNOs solely using the Red Compartida increased from 43% to 61%, which confirms that Red Compartida is important for the commercialization and development of the MVNO market.

In its annual report on the market (2023), the IFT conducted a survey among the MVNOs regarding their perception and use of Red Compartida with 83% of the respondents pointing out positive impacts, among which the following stand out:

- increase in user experience, and the expansion of markets, especially in highly marginalized areas;

- increase in coverage and quality of service,

- less dependence on roaming from traditional operators.

- 17% of the respondents said it had no usage of the Red Compartida because it is not a 5G network.

In parallel to the growth of MVNOs, the telecom regulator in Mexico (IFT), has also noted in its report, that the sector has become more competitive, as measured by the Herfindahl-Hirschman Index (HHI) for mobile telephony services. The HHI has decreased from 5,166 in year 2016 to 4,017 at the end of 2023.

Chart: From IFT’s report: Evolution in the contracting of the mobile telephony service Supply-Demand: a Comparative Vision 2016 vs 2023.

In addition, the pricing in the market has followed and in 2023 a greater number of GB were offered at lower prices, causing consumption to increase, according to the report’s evaluation.